Economic History & Future Predictions

Universal Basic Income: Pros, Cons, and Whether Free Money Can Save the Economy

AFFILIATE DISCLOSURE: This site does not currently have affiliate partnerships. All content is independently researched and written to provide you with accurate, unbiased financial information.

Could giving every citizen a regular, unconditional paycheck — no strings attached — solve poverty, cushion the blow of automation, and simplify the welfare state? Or would it trigger runaway inflation, drain government budgets, and discourage people from working?

Universal Basic Income (UBI) is one of the most hotly debated economic policies of the modern era. It touches on the most fundamental questions about the relationship between work, money, and human dignity. And as artificial intelligence reshapes the labor market at an accelerating pace, the debate has moved from academic seminars to congressional hearings and Silicon Valley boardrooms.

In this comprehensive guide, we break down exactly what UBI is, what the latest real-world evidence shows, and what it would mean for your finances and the broader economy.

What Is Universal Basic Income?

Universal Basic Income is a government program that provides all citizens with a regular, unconditional cash payment — regardless of employment status, income level, or personal circumstances.

| Characteristic | What It Means |

|---|---|

| Universal | Every citizen receives it, not just those in poverty or unemployment |

| Unconditional | No work requirement, no means test, no strings attached |

| Regular | Paid on a consistent schedule, typically monthly |

| Cash-based | Paid as money, not vouchers or in-kind benefits |

The idea is far older than most people realize. Thomas Paine proposed a form of universal income in 1796. Martin Luther King Jr. called for a guaranteed income in 1967. Richard Nixon’s version nearly passed Congress in 1970 and 1971. What’s new is the urgency — driven by AI, automation, and the growing gaps in existing safety nets.

The Case For UBI

1. A Direct Attack on Poverty

By guaranteeing every citizen a baseline income, UBI provides a financial floor below which no one can fall — effectively reducing extreme poverty, homelessness, and food insecurity in a single programmatic stroke rather than through a patchwork of overlapping benefits.

2. A Safety Net for the Age of Automation

As AI displaces workers across industries, UBI offers a structural solution — a permanent cushion providing financial security and time to retrain. Policy analysts warn of a dangerous “Valley of Death” — the transition period between the onset of widespread AI displacement and the implementation of comprehensive support — where the exponential speed of AI development significantly outpaces the linear speed of legislative action. (GovFacts)

3. Encouraging Entrepreneurship and Risk-Taking

A guaranteed income removes the existential financial fear that stops many people from starting businesses or pursuing creative work. With basic income as a safety net, more people can afford to take the economic risks that drive innovation and growth — a point that resonates with both progressive and libertarian supporters of UBI.

4. Simplifying the Welfare State

Modern welfare systems are notoriously complex and expensive to administer, riddled with arbitrary eligibility cutoffs and bureaucratic inefficiency. UBI could replace dozens of overlapping programs with a single, streamlined payment — reducing overhead, eliminating the stigma of means-tested benefits, and ensuring no eligible person falls through administrative cracks.

5. Stimulating Local Economies

Putting more money directly into the hands of lower-income citizens — who tend to spend a higher proportion of their income locally — acts as a grassroots economic stimulus, boosting demand in communities that need it most, rather than concentrating gains at the top of the income distribution.

6. Mental Health as a Public Health Intervention

The most consistent finding across all pilot studies is the improvement in mental health. Financial scarcity functions as a “cognitive tax,” reducing decision-making bandwidth and increasing anxiety. By alleviating this pressure, UBI has been shown to reduce anxiety, depression, and domestic violence — making it as much a public health intervention as an economic one. (GovFacts)

The Case Against UBI

1. The Cost Is Staggering

A $1,000 per month UBI for all adult U.S. citizens would cost approximately $2.8–3 trillion per year — equivalent to the entire current discretionary and mandatory federal spending outside of entitlements. For scale: U.S. corporations executed more than $1 trillion in stock buybacks over the 12 months through September 2025 — roughly one-third of the annualized tab for a national UBI. (Newsweek) Funding UBI would require massive tax increases, significant program cuts, or a dramatic expansion of the national debt.

2. Inflation Risk

If UBI injects large amounts of new money into an economy where housing, healthcare, and energy supply are constrained, it could drive up prices — potentially wiping out the purchasing power gains UBI was supposed to provide. If cash is handed out into markets where supply is tight, there is a real risk of funding landlords and utilities more than families. (Newsweek)

3. The Work Disincentive Question Is Genuinely Complicated

The largest U.S. UBI study to date — backed by Sam Altman and OpenAI — provided $1,000 per month to 1,000 low-income participants in Texas and Illinois for three years. The study found a moderate reduction in labor supply: recipients were 2 percentage points less likely to be employed and worked an average of 1.3 to 1.4 fewer hours per week than the control group, with total household income (excluding the transfer) dropping by approximately $1,500 per year. (GovFacts) Critics cite this as evidence UBI discourages work. Supporters counter that three years is not enough time to capture the full behavioral adaptation of a permanent, universal program.

4. Risk to Vulnerable Groups

If UBI replaces targeted welfare programs, people with above-average needs could end up worse off. A flat payment adequate for a healthy single adult may be wholly inadequate for a family with a disabled child, a person requiring ongoing medical care, or someone in a high cost-of-living city.

5. Political and Implementation Complexity

As of 2025, no country has fully implemented a nationwide Universal Basic Income program. (Newsweek) The political coalition required to pass, fund, and sustain a true UBI at national scale — across elections and economic cycles — has never been successfully assembled anywhere in the world.

What the Evidence From Real-World Pilots Actually Shows

Between 2017 and 2025, at least 122 pilots across 33 U.S. states and the District of Columbia evaluated a guaranteed basic income, allocating $481 million in payments to more than 40,000 recipients. (American Enterprise Institute)

| Location | Program | Key Finding |

|---|---|---|

| Finland | 2017–2018: €560/month to 2,000 unemployed people | Higher wellbeing and mental health; modest employment improvement vs. control group |

| Alaska, USA | Annual Permanent Fund Dividend since 1982 | Consistently lowest poverty rates in U.S.; minimal negative effect on labor participation |

| Stockton, CA | $500/month to 125 residents for 24 months | Full-time employment among recipients actually increased; significant mental health gains |

| Texas & Illinois (OpenResearch) | $1,000/month to 1,000 low-income participants for 3 years | Moderate reduction in hours worked; improved wellbeing and health outcomes |

| Kenya (GiveDirectly) | Long-term UBI trial in rural villages | Strong positive effects on consumption, assets, and wellbeing; no significant reduction in work |

| Wales, UK | £1,600/month to 600+ young care-leavers | Improved mental health; increased educational participation; some concerns about work incentives |

| Cook County, IL | $500/month to 3,250 families for 2 years | Significant improvements in financial stability; County approved $7.5M for continued programming in FY2026 |

Among the 30 randomized controlled trial pilots with published employment outcomes, the mean effect of guaranteed basic income is an increase of 0.8 percentage points in the share employed (American Enterprise Institute) — though larger, higher-quality trials show a modest negative employment effect. The honest summary: the evidence is genuinely mixed on employment, but consistently positive on wellbeing and poverty reduction.

How Could UBI Actually Be Funded?

Funding is where UBI proposals face their toughest scrutiny. The main mechanisms under serious discussion include:

- Value-Added Tax (VAT): The most commonly proposed mechanism. Economic modeling suggests a budget-neutral UBI could be funded with a 1.5% consumption tax increase if it replaced the existing welfare system — but a $1,000/month UBI would require a much larger 19.3% rise in consumption taxes. (LSE)

- Wealth Tax: A progressive annual tax on net worth above a threshold, redistributed as universal payments. Technically feasible; politically contentious and constitutionally uncertain in the U.S.

- Carbon or Resource Tax: Modeled on Alaska’s oil dividend — taxing the use of public resources (carbon emissions, land value, data extraction) and redistributing the proceeds universally.

- Financial Transactions Tax: A small levy on stock, bond, and derivatives trades that would generate significant revenue given the volume of financial market activity.

- Consolidation of Existing Programs: Replacing overlapping welfare programs with a single universal payment, capturing administrative savings — though this approach risks cutting vital targeted support for people with above-average needs.

- An “AI Dividend”: An emerging 2025–2026 concept where companies that profit most from automation pay into a fund redistributed to displaced workers. The productive middle ground for 2026 and beyond looks less like a moon-shot UBI and more like a targeted “AI dividend” that scales with measured exposure to automation, paired with investments in housing, power, and care. (Newsweek)

The Bipartisan History of UBI — It’s Not Just a Left-Wing Idea

UBI’s political lineage spans the ideological spectrum in ways that might surprise you:

- Thomas Paine (1796): Proposed universal payments from a land tax as compensation for the privatization of common resources

- Milton Friedman (1962): Proposed a “negative income tax” — a conservative version of UBI — to replace the bureaucratic welfare state

- Richard Nixon (1969): Proposed a Family Assistance Plan that would have guaranteed income to all families; it passed the House twice before stalling in the Senate

- Martin Luther King Jr. (1967): Argued a guaranteed income was the most direct solution to poverty

- Barack Obama (2016): Suggested the social compact would need updating as AI and automation advanced

- Sam Altman/OpenAI (2022–2025): Funded the largest randomized controlled UBI trial in U.S. history

The idea has survived across political eras precisely because it solves real problems that neither pure markets nor targeted welfare programs have fully resolved.

How This Impacts You

- If you’re in a job vulnerable to automation: The UBI debate is really a debate about what society owes you during the transition. Even without UBI, understanding the policy landscape helps you advocate for yourself — through skills development, union protections, or retraining programs — rather than waiting for a policy that may or may not arrive in time.

- If you’re a low-income household: The expansion of guaranteed income pilots across the U.S. is real and ongoing. If you live in a city or county running a pilot, you may already be eligible or become eligible for a local program — worth researching directly at guaranteedincome.us.

- If you’re a taxpayer: How UBI is funded matters enormously. A VAT-funded UBI effectively taxes consumption — meaning higher earners pay more in absolute dollars, but lower earners pay a higher share of their income. Understanding the funding mechanism is just as important as understanding the payment itself.

- If you’re an investor or business owner: A world with UBI — even a partial or regional version — is a world with more consumer purchasing power at the bottom of the income distribution. Businesses serving lower-income consumers, local services, and everyday goods would see direct demand benefits.

- If you’re a parent or educator: The evidence from pilots consistently shows improvements in children’s outcomes when their parents receive guaranteed income — better nutrition, lower household stress, higher educational attainment.

Frequently Asked Questions

1. Would UBI replace existing welfare programs?

That depends entirely on the design. Some proposals replace existing programs with a single universal payment; others add UBI on top of existing benefits. Caution is warranted in assuming pilots translate cleanly to a permanent, universal, nationwide program (American Enterprise Institute) — the funding and design choices made at scale would determine whether vulnerable groups are better or worse off than under the current system.

2. How would a national UBI be funded?

The most discussed mechanisms include a value-added tax, a wealth tax on high net-worth individuals, a carbon or resource tax, a financial transactions tax on Wall Street activity, consolidation of existing welfare programs, or a new “AI dividend” tax on companies that profit from automation. No single funding mechanism has achieved political consensus.

3. Would UBI cause inflation?

Potentially, yes — particularly in housing and healthcare where supply is constrained. However, if UBI is funded through redistribution rather than new money creation, the net inflationary effect is more limited. The design of the program — and what it replaces — matters more than the headline payment amount.

4. Has UBI ever been tried at a national scale?

As of 2025, no country has fully implemented a nationwide Universal Basic Income program. Alaska’s Permanent Fund Dividend is the closest real-world example at a large scale, though it is funded by oil revenues and is supplemental rather than a living wage.

5. Is UBI a left-wing or right-wing idea?

Neither — and both. The idea has been championed by progressive poverty advocates, libertarian welfare-state critics, conservative economists like Milton Friedman, and tech entrepreneurs like Sam Altman. It has opponents across the spectrum too. The policy itself is ideologically neutral; what separates supporters from critics is how it’s funded, what it replaces, and how large the payment is.

Internal Resources Worth Reading

- The Impact of AI on the Global Economy: Boom, Bust, or Both?

- The Rise of Economic Populism: What It Means for Money and Markets

- How the Federal Reserve Controls Inflation

- What Happens If the Dollar Loses Reserve Currency Status?

External Sources

The Gold Standard Debate: Should We Return to Backed Money?

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Explore the gold standard debate — should modern economies return to gold-backed money, or is fiat currency the better path forward?

Introduction: Why The Gold Standard Debate Still Matters Today

If there’s one topic that never seems to lose its shine in economic circles, it’s the gold standard debate. From YouTube finance influencers to policymakers and everyday savers, many are asking: Should we bring back money backed by gold?

The question isn’t just about nostalgia for shiny coins or distrust in “paper money.” It cuts to the heart of how value is created, stored, and protected in our financial system. In an age of inflation fears, digital currencies, and mounting government debt, people are searching for a system that feels real again — one grounded in something tangible.

So, should we go back to the gold standard? Or has the world moved beyond it for good?

Let’s unpack the history, arguments, and real-world implications — and see how this debate connects directly to your financial life today.

️ What Was the Gold Standard?

The gold standard was a monetary system where a country’s currency was directly tied to a specific amount of gold. For example, under the U.S. gold standard of the early 20th century, $35 equaled one ounce of gold. That meant every dollar in circulation could theoretically be exchanged for gold held in government vaults.

This system limited how much money could be created. The government couldn’t print more money unless it had more gold to back it up. Supporters say that kept inflation low and disciplined public spending.

Types of Gold Standards:

- Classical Gold Standard (1870–1914): Money was fully convertible to gold, and global trade was stable.

- Gold Exchange Standard (1925–1931): Countries held foreign currencies (like U.S. dollars or British pounds) backed by gold.

- Bretton Woods System (1944–1971): The U.S. dollar was pegged to gold, and other nations pegged their currencies to the dollar.

When President Richard Nixon ended dollar convertibility to gold in 1971, the world entered the era of fiat money — currency not backed by a commodity, but by government decree and economic trust.

⚖️ Fiat Money vs. Gold-Backed Money: What’s the Real Difference?

The debate often boils down to control versus stability.

Feature Gold-Backed Money Fiat Money

Value Basis Linked to a physical commodity (gold) Based on government trust and regulation

Money Supply Control Limited by gold reserves Determined by central banks

Inflation Control Naturally constrained Requires policy discipline

Economic Flexibility Restricted (limited stimulus) Highly flexible

Historical Stability Long-term stable prices Prone to inflation and crises

Crisis Response Slow — limited tools Quick — central banks can print money

Fiat systems allow nations to respond to crises like COVID-19 or financial crashes by injecting liquidity. But critics argue this power often leads to debt bubbles, currency devaluation, and inequality.

“Gold Standard vs. Fiat Money Comparison Template”

Use this simple template to compare how each system affects you personally.

Reflect and fill in your own observations.

Category Gold Standard System Fiat System (Today’s Money) Your Reflection

Money Creation Backed by physical gold reserves Created digitally or through lending _______________

Inflation Impact Historically low Often higher, depends on policy _______________

Savings Power Stable value over time Subject to erosion by inflation _______________

Debt and Borrowing Limited government borrowing High debt flexibility _______________

Economic Growth Slower but steadier Faster but volatile _______________

Financial Stability Hard money discipline Dependent on trust and regulation _______________

Personal Comfort Level Tangible security Policy-driven confidence _______________

Tip: Use this template as part of your personal financial education journal — track how your beliefs about money evolve as you understand the system better.

The Case For the Gold Standard

Advocates believe that returning to gold-backed money could restore trust and discipline in the economy. Here are the key arguments:

1. Inflation Control

Because money creation would be limited by gold reserves, governments couldn’t inflate away debt or overspend.

2. Fiscal Discipline

The gold standard forces governments to live within their means — reducing reckless deficit spending and long-term debt accumulation.

3. Stable Value

Over centuries, gold has retained its value better than any fiat currency. This stability can restore confidence for savers and investors.

4. Global Trust

A universal gold-based system could stabilize international exchange rates and reduce speculative currency wars.

As economist Milton Friedman once said:

“Inflation is taxation without legislation.”

The gold standard, in theory, prevents that kind of hidden tax.

The Case Against the Gold Standard

Critics argue that while gold may shine, it can also trap economies in rigidity.

1. Limited Flexibility

In times of crisis, such as the Great Depression, the gold standard prevented central banks from increasing the money supply to revive the economy.

2. Deflation Risk

When money supply can’t expand, prices fall — leading to wage cuts, job losses, and economic stagnation.

3. Resource Dependence

Economic growth would depend on mining more gold — not innovation or productivity.

4. Unequal Gold Distribution

Countries rich in gold (like the U.S. post–World War II) would dominate, leaving others vulnerable to external shocks.

5. Not Fit for the Digital Age

Modern economies rely on electronic transfers, derivatives, and dynamic credit systems — not physical metal locked in vaults.

A Balanced View: Could a Partial Gold Standard Work?

Some economists propose a hybrid system — where currencies are partially backed by gold, digital assets, or a commodity basket.

This could combine the stability of hard assets with the flexibility of fiat systems.

For example:

- The International Monetary Fund (IMF) has explored “Special Drawing Rights” (SDRs) as a diversified reserve currency.

- Central banks could issue digital currencies (CBDCs) with fractional gold backing to maintain public confidence.

Such innovations could represent a “Gold Standard 2.0” — not a step backward, but an evolution toward responsible money creation.

Trending Question: Would Returning to the Gold Standard Stop Inflation?

This is one of the most common questions driving the gold standard debate with strong arguments on both sides.

In theory, yes — tying money to gold would limit inflation by limiting the money supply and imposing fiscal discipline. But in practice, it is not guaranteed to stop inflation and could limit economic growth and increase unemployment during downturns resulting in economic instability and a loss of monetary policy flexibility to manage it.

The U.S. Congressional Research Service (CRS) notes that the Great Depression worsened because the gold standard restricted government action (source: crsreports.congress.gov).

Meanwhile, the Federal Reserve explains that fiat flexibility has helped stabilize output and prices since 1971 (federalreserve.gov).

So, while gold backing could discipline policy, it’s not a magic cure. The real solution lies in responsible governance, not just shiny metal.

What It Means for You: How This Debate Impacts Your Finances

Even if we never return to a gold standard, understanding this debate helps you make smarter decisions.

✅ 1. Inflation Awareness

Knowing how fiat systems work helps you protect your savings with inflation-hedged assets (like TIPS, real estate, or diversified ETFs).

✅ 2. Diversified Investing

Gold can be part of a balanced portfolio — not because of nostalgia, but as a hedge against monetary uncertainty.

✅ 3. Debt Perspective

In fiat systems, debt is a feature, not a flaw. Understanding this lets you navigate credit systems and government borrowing logically.

✅ 4. Critical Thinking

When politicians or influencers promise “sound money” through gold, you’ll be able to ask: How would that affect jobs, liquidity, and growth?

To deepen your understanding:

Internal Links (TheMoneyQuestion.org)

- Who Really Controls the Money? A Look at Central Banks

- The Debt Myth: Why Government Borrowing Isn’t Like a Household Budget

External Links

-

Federal Reserve History – The End of the Gold Standard https://www.federalreservehistory.org/essays/gold-standard

Overview from the Federal Reserve on why the U.S. ended gold convertibility in 1971 and the long-term economic implications. -

Congressional Research Service (CRS) – Returning to the Gold Standard: Historical and Policy Perspectives

https://crsreports.congress.gov/product/pdf/R/R43890

A nonpartisan U.S. government analysis explaining the potential effects of reinstating a gold-backed monetary system. -

Investopedia – What Is the Gold Standard?

→ https://www.investopedia.com/terms/g/goldstandard.asp

Educational reference summarizing the gold standard’s history, advantages, and disadvantages in accessible language.

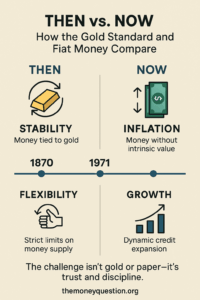

“Then vs. Now: How the Gold Standard and Fiat Money Compare”

Sections:

- Visual timeline (1870 → 1971 → Today)

- Icons for stability, inflation, flexibility, and growth

- Key takeaway: “The challenge isn’t gold or paper — it’s trust and discipline.”

- Add footer: themoneyquestion.org

Key Takeaways

- The gold standard offered stability, but limited flexibility.

- Fiat money offers flexibility, but risks inflation and overspending.

- The best system may blend discipline with innovation.

- Understanding money’s foundation empowers smarter financial choices.

Conclusion: Beyond the Gold Standard Debate

The gold standard debate isn’t just academic — it’s about who controls money, and how that control affects your life.

Whether we back currency with gold, digital code, or trust, the key issue remains accountability.

If citizens understand money creation, demand transparency, and make informed personal choices, the system becomes stronger — whatever form it takes.

Gold isn’t the answer. But the discipline it represents might be the one lesson modern money still needs.

FAQs: The Gold Standard Debate

1. What was the purpose of the gold standard?

The gold standard aimed to ensure monetary stability by tying each unit of currency to a fixed quantity of gold. This limited governments from creating money arbitrarily and helped control inflation. It also made international trade smoother because exchange rates were predictable and trusted.

2. Why did the U.S. abandon the gold standard?

The U.S. left the gold standard in 1971 when President Nixon ended convertibility to preserve economic flexibility. Global trade imbalances and postwar spending made it impossible to maintain fixed gold prices. Moving to fiat money allowed the government and Federal Reserve to respond more effectively to inflation, unemployment, and recession pressures.

3. Would a return to gold stop inflation permanently?

A gold-backed system could reduce inflation by limiting the money supply, but it wouldn’t eliminate it entirely. Prices also depend on productivity, wages, and global demand. Historically, gold standards have sometimes caused deflation, which can be just as harmful as inflation.

4. Is gold-backed money safer than fiat money?

Gold-backed money can feel safer because its value is linked to a tangible asset rather than government trust. However, this safety comes at the cost of flexibility — governments can’t easily stimulate growth or respond to crises. Fiat systems rely on policy discipline instead of metal reserves for stability.

5. Can digital currencies be gold-backed?

Yes, several new technologies allow for digital currencies partially backed by gold. Central Bank Digital Currencies (CBDCs) or stablecoins could use gold reserves to ensure value stability while allowing digital efficiency. This hybrid model combines traditional trust with modern innovation.

6. What caused the Great Depression under the gold standard?

During the Great Depression, the gold standard limited how much money governments could create to boost their economies. As prices and wages fell, deflation deepened the downturn. Countries that left the gold standard earlier — like the U.K. — recovered faster than those that stayed tied to it.

7. Does any country use the gold standard today?

No major economy operates on the gold standard today; all use fiat money issued by central banks. However, countries like Switzerland and Singapore maintain strong gold reserves as part of their financial security strategy. Gold remains an important reserve asset, even without direct convertibility.

8. Should investors buy gold now?

Gold can be a good diversification tool, especially during times of inflation or market uncertainty. Financial advisors often recommend allocating 5–10% of your portfolio to gold or similar assets. It’s not about betting on a gold standard comeback — it’s about hedging against fiat volatility.

9. What are the pros of fiat money?

Fiat money gives governments and central banks the flexibility to manage the economy, fund public programs, and respond to crises. It allows for credit expansion and innovation, which drive growth. The challenge is maintaining discipline so that flexibility doesn’t lead to runaway inflation.

10. What’s the biggest takeaway from the gold standard debate?

The real question isn’t whether we should return to gold — it’s whether we can create a responsible and transparent monetary system. Sound money depends more on good governance and informed citizens than on any metal. Understanding both systems empowers you to make better financial and policy judgments.

Affiliate Disclosure

Some links on this page may be affiliate links. This means we may earn a small commission at no extra cost to you if you purchase through them.

Disclaimer: The content provided is for informational purposes only and is not a substitute for professional financial or legal advice.

A Brief History of Money and Banking

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Discover how money and banking evolved—from ancient trade to banking in the Middle Ages—and what it reveals about today’s financial system.

Introduction: The Long Journey of Money and Banking

Money didn’t start as coins, paper, or digital code. It began as trust. From seashells and salt to gold coins and digital ledgers, the story of money is really a story about how humans organize trust, power, and value.

In this post, we’ll explore banking in the Middle Ages, the roots of modern finance, and what these historical lessons can teach you about money management today.

By the end, you’ll understand:

-

How early banking systems laid the groundwork for today’s economy

-

Why medieval innovations like bills of exchange changed everything

-

How understanding the past can help you make smarter financial decisions today

Before the Banks: Barter and Early Exchange

Long before credit cards and online transfers, humans relied on barter—trading goods and services directly.

But barter was inefficient. A farmer with wheat might not need a fisherman’s catch. This “double coincidence of wants” problem forced societies to find a common medium of exchange—something durable, portable, and universally accepted.

The Birth of Commodity Money

-

Early forms of money included cattle, shells, salt, silver, and gold.

-

By 2500 BCE, the Sumerians recorded transactions on clay tablets, one of the earliest examples of accounting.

-

The Code of Hammurabi (circa 1750 BCE) outlined interest rates and loan contracts, showing how old money management really is.

Money simplified trade, but it also required new systems of record-keeping, lending, and regulation—the precursors of banking.

Temples, Merchants, and the First “Banks”

Before there were bankers, there were priests. In Mesopotamia, temples held grain and precious metals for safekeeping. People deposited their valuables, and the temple lent resources to others—collecting interest as profit.

This early system mirrored modern banking principles:

-

Deposits: People entrusted goods to a trusted intermediary.

-

Loans: Those resources were lent to others.

-

Interest: The intermediary profited by lending at a higher rate.

By the time of ancient Greece and Rome, moneylenders—called trapezitai in Greek—handled deposits, loans, and currency exchange. In Rome, bankers (argentarii) even recorded transactions in ledgers similar to modern account books.

The Collapse of Rome and the Dormant Centuries

When the Roman Empire fell in the 5th century, Europe’s trade networks disintegrated. Roads decayed, cities emptied, and coins became scarce. The idea of “banking” all but disappeared.

But not everywhere.

In the Islamic world, scholars preserved and expanded financial knowledge. Islamic banking principles—rooted in partnerships and profit-sharing rather than interest—thrived from Baghdad to Cordoba.

These ideas would later influence European banking practices during the Middle Ages.

Banking in the Middle Ages: The Birth of Modern Finance

Banking in the Middle Ages—marks a turning point in financial history.

Between the 11th and 15th centuries, European commerce revived, trade routes reopened, and merchants needed safer, faster ways to move money across distances. Carrying gold was dangerous and inefficient, so they turned to paper instruments, early credit systems, and trusted financial intermediaries.

The Italian Banking Renaissance

The story begins in Italy, the heart of medieval trade. Cities like Venice, Florence, and Genoa became bustling hubs of commerce—and innovation.

Key Developments:

-

Bills of Exchange: Merchants could pay with paper instead of coins. These acted like early checks, allowing someone to deposit money in one city and withdraw it in another.

-

Merchant Banks: Families like the Medici of Florence created banking houses that offered currency exchange, loans, and investment services.

-

Double-Entry Bookkeeping: A revolutionary accounting method (first codified by Luca Pacioli in 1494) made it easier to track profits and losses accurately.

This was the dawn of financial literacy. Banking became systematic, and the word “bank” itself derived from banca—the Italian word for “bench,” where moneylenders once did business.

Faith, Trust, and Regulation in Medieval Finance

In the Middle Ages, money was not just economics—it was morality.

The Catholic Church forbade usury (charging interest), believing it sinful to profit from lending. But trade demanded credit, so bankers found creative ways around the rule—charging “fees” or “exchange rates” instead of explicit interest.

Meanwhile, trust became the currency of commerce. Banks held vast power but depended on reputation. A single rumor could trigger a medieval bank run, collapsing fortunes overnight—just as it can today.

Case Study: The Medici Bank

The Medici Bank (1397–1494) is often considered the blueprint of modern banking.

Founded by Giovanni di Bicci de’ Medici, it grew into a financial empire spanning Europe. The Medici family financed kings, popes, and trade expeditions—while pioneering practices like:

-

Branch banking (offices across cities)

-

Letters of credit (predecessors to modern wire transfers)

-

Partnership management structures

However, political entanglements and risky loans eventually led to the bank’s downfall—a timeless reminder that over-leverage and corruption destroy even the strongest institutions.

The Birth of National Banks

As Europe entered the Renaissance, monarchs realized they needed centralized systems to finance wars and trade. This led to additional developments to money and banking as financiers adapted to changing requirements of users of the financial system.

The Bank of Amsterdam (1609) became one of the first public banks, followed by the Bank of England (1694), which introduced the concept of fractional reserve banking—holding only a fraction of deposits in reserve while lending out the rest.

This innovation fueled economic growth but also created systemic risk, linking credit cycles, inflation, and government debt in ways that shape our world today. This led to developments in record keeping, credit assessment

From Paper to Policy: The Age of Central Banking

As trade globalized, so did money. Governments standardized currencies, issued banknotes, and began regulating credit and interest.

By the 19th century, central banks—like the Bank of France and later the U.S. Federal Reserve (1913)—emerged to stabilize economies, issue currency, and manage crises.

Yet, the roots of their power trace directly back to banking in the Middle Ages, when trust, record-keeping, and liquidity management first became financial science.

How Historical Banking Shapes Your Finances Today

Understanding this history isn’t just trivia—it’s empowerment.

Many modern banking practices—credit scoring, interest, savings accounts, and loans—stem from ideas refined over centuries. Knowing this can help you:

-

Make smarter borrowing decisions

-

See how banks manage (and sometimes manipulate) money supply

-

Recognize how trust and regulation shape financial stability

For instance, just as medieval merchants diversified trade routes, modern investors diversify portfolios. The principles endure even as the tools evolve.

Controversial Question: Should We Return to Gold-Backed Money?

One trending debate asks: “Would a return to gold-backed money restore financial stability?”

The gold standard, once common after the Renaissance, tied currency value to physical gold. Some argue it prevents inflation; others say it limits economic flexibility.

History shows that while gold systems created stability, they also restricted growth—especially in times of crisis. The flexibility of credit and monetary policy (originating from medieval and Renaissance banking) enabled societies to rebuild after wars, pandemics, and depressions.

Takeaway: Stability requires trust, not just metal. Sound governance matters more than what backs the currency.

Downloadable Freebies

1. Timeline of Money & Banking Evolution Worksheet

Visualize the transformation of trade and finance—from bartering to digital currency.

➡️ Download the Timeline Worksheet here (insert download link on site)

2. Money Systems Through History Cheat Sheet

A one-page quick reference summarizing key milestones, from Mesopotamian temples to crypto economies.

➡️ Download the Cheat Sheet here

{kind=link}

Internal Links

To deepen your understanding, explore related posts on TheMoneyQuestion.org:

-

The Gold Standard Debate: Should We Return To Backed Money? (Coming Soon)

- The End of Fractional Reserve Banking? Here’s What We Know

External Sources

Conclusion: The Past Is the Blueprint for the Future

The story of money and banking is the story of civilization itself. From the grain banks of Mesopotamia to the Medici in Florence, from paper notes to digital ledgers, one thing remains constant: money is a system of trust.

Understanding banking in the Middle Ages shows that our financial system—while complex—is built on simple human principles of trust, record-keeping, and mutual benefit.

Whether you’re managing a household budget or analyzing global finance, knowing where money came from helps you navigate where it’s going.

FAQs

1. What was banking in the Middle Ages like?

It revolved around merchant families, bills of exchange, and trust-based credit systems—especially in Italy and Northern Europe. It was a time of significant innovation, though practices were constrained by religious prohibitions.

2. Who were the first bankers?

This question depends on how broadly you define “banking”, as the practice evolved over thousands of years. Temples in Mesopotamia (~2000BC), The Knights Templar (12th – 13th Century), and merchants in Renaissance Italy (14th – 15th Century) are considered the world’s earliest bankers.

3. What replaced barter systems?

Commodity money—like silver, gold, and salt—eventually evolved into coins and paper money.

4. Why was usury banned in medieval Europe?

The Church viewed charging interest as immoral, though trade required credit, leading to workarounds. Bankers found ways to circumvent this ban by:

- imposing a “fine” for late repayment, with the understanding that the debtor would always pay late.

- using contracts like the bill of exchange and adjusting the exchange rate to incorporate an implicit interest payment.

5. Who invented double-entry bookkeeping?

Luca Pacioli formalized it in 1494; this system remains the foundation of modern accounting.

6. What led to the fall of the Medici Bank?

Political risk, bad loans, and mismanagement caused its collapse.

7. How did banking spread beyond Italy?

Through trade networks into France, England, and the Low Countries, setting the stage for national banks.

8. What was the first central bank?

- The world’s oldest surviving central bank, and the one widely recognized as the first, is the Sveriges Riksbank (the Swedish Riksbank). It was founded in Sweden in 1668. The Bank of England (1694) is often credited as the second central bank.

9. How did medieval banking influence today’s system?

- Medieval banking, primarily led by Italian merchant families and religious orders, provided the foundational tools and concepts that are indispensable to the modern financial system. The core contribution was the shift from a physical, coin-based economy to a credit-based, document-driven system.

10. What can modern savers learn from history?

Here are four major lessons drawn from past financial crises, economic downturns and centuries of human behaviour:

- Everyone should have a Cash Emergency Fund. Failure to have access to cash make people more vulnerable to events like The Great Depression, the 2008 financial crisis and the COVID-19 economic shock.

- Diversification across different asset classes, geographic regions and industries is a must so no single event can wipe out your entire portfolio.

- Avoid overleveraging and speculation. Be cautious with debt, especially consumer debt.

- Pay yourself first. This is the ancient discipline of thrift. Make saving automatic and non-negotiable.

Affiliate Disclosure

This post may contain affiliate links. If you purchase through these links, TheMoneyQuestion.org may earn a small commission—at no extra cost to you.

Content is for informational purposes only and not a substitute for advice from certified financial professionals.

The 2008 Financial Crisis vs Today: Are We Heading For Another Financial Meltdown?

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Is another financial crisis looming? Compare the 2008 meltdown to today’s economic risks—rising debt, Inflation, and market volatility. Learn how to protect your finances and what warning signs to watch.

Introduction

The 2008 financial crisis was one of the worst economic disasters in modern history, triggered by reckless lending, a housing bubble, and the collapse of major financial institutions. Over a decade later, concerns are rising again—soaring Inflation, mounting debt, and geopolitical instability have many asking: Are we heading for another financial meltdown?

In this in-depth analysis, we’ll compare the 2008 crisis to today’s economic landscape, examine key risk factors, and explore how investors can safeguard their wealth.

The 2008 Financial Crisis: A Quick Recap

The 2008 crisis was primarily caused by:

- Subprime Mortgage Lending – Banks issued high-risk loans to borrowers with poor credit, betting on ever-rising home prices.

- Securitization & Derivatives – Toxic mortgage-backed securities (MBS) and credit default swaps (CDS) spread risk across the global financial system.

- Bank Failures & Bailouts – Lehman Brothers collapsed, while institutions like AIG and Citigroup required massive government rescues.

- Global Recession – Stock markets crashed, unemployment spiked, and economies worldwide entered prolonged downturns.

The aftermath led to stricter regulations like the Dodd-Frank Act and higher capital requirements for banks. But have these measures made the financial system safer today?

Today’s Economic Landscape: Key Risk Factors

- Soaring National & Consumer Debt

- U.S. National Debt: Over **34trillion∗∗(vs. 34trillion∗∗(vs. 10 trillion in 2008). (U.S. Treasury)

- Consumer Debt: Credit card debt hit $1.13 trillion in 2024, with rising delinquencies. (Federal Reserve)

- Inflation & Central Bank Policies

- Post-pandemic Inflation peaked at 9.1% in 2022, the highest in 40 years.

- The Federal Reserve raised interest rates aggressively, but cuts may come in 2024—will this reignite Inflation?

- Commercial Real Estate (CRE) Crisis

- Remote work has devastated office space demand.

- Over $1.5 trillion in CRE loans will mature by 2025—many at higher rates. (Moody’s Analytics)

- Banking Sector Vulnerabilities

- The 2023 collapse of Silicon Valley Bank (SVB) and Signature Bank exposed risks in regional banks.

- Rising loan defaults could trigger another liquidity crisis.

- Geopolitical Risks & Market Volatility

- Wars, trade tensions, and supply chain disruptions add uncertainty.

- Stock markets remain near all-time highs—could a correction be coming?

Key Differences Between 2008 and Today

Factor2008 CrisisToday’s Risks

Trigger housing collapse, subprime mortgages, Inflation, debt bubbles, and CRE weaknesses.

Banking Health Weak capital reserves, Lehman collapsed. Stronger, but regional banks were vulnerable.

Regulations Loose pre-2008, tightened after Some rollbacks, but stricter oversight.

Government Role Massive bailouts (TARP) Fed balance sheet still inflated

Are We Heading for Another Meltdown?

While today’s risks differ from 2008, warning signs exist:

✅ Debt levels are unsustainable (government, corporate, and consumer).

✅ Commercial real estate could spark bank failures.

✅ Inflation remains a threat if the Fed cuts rates prematurely.

However, banks are better capitalized, and regulators are more vigilant. A full-scale 2008-style crash seems less likely—but a severe recession or market correction is possible.

How to Protect Your Finances

- Diversify Investments – Avoid overexposure to stocks; consider bonds, gold, and real estate.

- Reduce High-Interest Debt – Pay down credit cards and refinance loans.

- Build an Emergency Fund – Aim for 3-6 months of living expenses.

- Monitor the Fed’s Moves – Interest rate changes will impact markets.

10 Related FAQs

- What caused the 2008 financial crisis?

The collapse of subprime mortgages, banks’ excessive risk-taking, and Lehman Brothers’ failure triggered the meltdown.

- Could a bank collapse like 2008 happen again?

While major banks are stronger, regional banks (like SVB in 2023) remain vulnerable.

- How does today’s Inflation compare to 2008?

Inflation was moderate in 2008 (~5.6% peak), while 2022 saw 9.1%—the highest since 1981.

- Is the housing market in a bubble now?

Home prices have surged, but stricter lending standards make a 2008-style crash unlikely.

- What’s the most significant financial risk today?

Soaring national debt, commercial real estate defaults, and geopolitical instability.

- Should I move my money to cash?

Holding some cash is wise, but long-term investors should stay diversified.

- Are stocks overvalued now?

Some analysts warn of high P/E ratios, but timing the market is risky.

- How can I prepare for a recession?

Reduce debt, increase savings, and avoid panic-selling investments.

- Will Bitcoin protect me in a crisis?

Crypto is volatile—gold and Treasury bonds are safer hedges.

- What’s the best investment during Inflation?

Real estate, commodities (gold, oil), and inflation-protected securities (TIPS).

SEO Keywords & Hashtags

Keywords:

- 2008 financial crisis vs today

- Are we in a financial bubble?

- Next economic crash prediction

- How to prepare for a recession

- Inflation and debt crisis

Hashtags:

#FinancialCrisis #EconomicCollapse #Inflation #StockMarket #Investing

Final Thoughts: While another 2008-style meltdown isn’t guaranteed, economic risks are rising. Stay informed, diversify your assets, and avoid panic-driven decisions.

Affiliate Marketing Disclosure

This post may contain affiliate links. If you make a purchase through these links, we may earn a commission at no extra cost to you. We only recommend products/services we believe in. Thank you for supporting our work!

The Pandemic’s Financial Maze: Insights from The Doom Loop

| Aspect | 2008 Crisis | Pandemic Crisis |

| Focus | Banks and mortgages | Economy, jobs, businesses |

| Interest Rates | Gradual cuts | Immediate drop to near-zero |

| Quantitative Easing | Stabilized banks | Broad liquidity injection |

| Bailouts | Banks and automakers | Businesses, states, cities |

| Programs | TARP | PPP, direct loans |

| Outcome | Slow recovery | Quick response, long risks |

The Economy in Chaos: How the Pandemic Started It All

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

When the pandemic hit, it felt like the economy slammed into a brick wall. Businesses shut down, people lost jobs, and everything seemed uncertain. That’s when the Federal Reserve stepped in to prevent an all-out collapse.

- What Did the Fed Do?: The Fed pulled out all the stops to keep things afloat. Interest rates were slashed to nearly zero, making borrowing money cheaper. They introduced quantitative easing (QE), where the Fed started buying assets to pump money into the system and prevent market freezes. Emergency loan programs were also rolled out to help businesses, cities, and financial institutions stay afloat.

- Big Finance’s Role: Big banks and investment firms were key players during this time. They helped stabilize things by distributing loans and offering financial support. But they also added fuel to the fire by relying on risky investments, making the financial system even more fragile.

What’s the Doom Loop All About?

The “doom loop” is the star of the book. It’s a vicious cycle where financial instability forces interventions like bailouts or QE, which then create even more risks down the line.

Low interest rates encourage banks and firms to take on more risk because borrowing is so cheap. A handful of big players controlling massive chunks of the market makes the system fragile. Financial institutions start expecting help whenever things go south, leading to risky behavior and a dependency on government interventions.

Takeaway: The doom loop shows how quick fixes can sometimes make long-term problems worse.

What the Book Does Well

There’s a lot to love about The Doom Loop. It’s well-researched, insightful, and explains tricky concepts in a way that doesn’t feel like a college textbook.

- Complex Topics Made Simple: The authors break down complicated financial policies into something even non-experts can understand. If you’ve ever wondered how QE or bailouts actually work, this book explains it clearly.

- Fair Critique of the Fed: Instead of just bashing the Federal Reserve, the book offers a balanced take. It gives credit where it’s due while pointing out areas where the Fed might’ve dropped the ball.

- Behind the Scenes of Big Finance: The book takes you into the world of big banks and investment firms, showing how their strategies can both stabilize and destabilize the economy.

Where the Book Could Do Better

No book is perfect, and The Doom Loop has a couple of areas where it could have gone further.

- A Little Too Technical at Times: Some parts lean heavily on financial jargon, which could make casual readers feel a bit lost.

- It’s All About the U.S.: While the focus on the U.S. financial system is understandable, it would’ve been great to see more comparisons with how other countries handled the pandemic.

Why It Matters Today

This book isn’t just a recap of what happened; it’s a warning and a guide for what we should watch out for in the future.

- Fixing the System: One big takeaway is that we need better regulations to keep the financial system stable. That means things like stricter rules on how much risk banks can take and more transparency about their practices.

- Breaking the Cycle: The dependency on government bailouts and interventions has created what’s known as a moral hazard. Financial institutions take risks because they expect to be rescued if things go wrong. That needs to change.

- Preparing for the Next Crisis: The pandemic taught us a lot about how fragile our systems are. By learning from what worked—and what didn’t—we can be better prepared for whatever comes next.

Takeaway: The lessons from this book aren’t just for economists or policymakers. They’re for anyone who wants to understand how financial systems impact all of us.

Wrapping It Up

The Doom Loop: The Fed and Big Finance in the Pandemic is an eye-opening look at how the financial world responded to one of the biggest crises of our time. It doesn’t shy away from tough questions and leaves readers with plenty to think about. If you’re curious about how monetary policy and big finance shape the world we live in, this book is a must-read.

FAQs

What exactly is the doom loop?

It’s a cycle where financial instability forces interventions like bailouts, which end up creating even more risks, leading to more instability.

How did the pandemic affect small businesses financially?

The Federal Reserve’s actions, like providing emergency loans and lowering interest rates, helped small businesses access funds to stay afloat during the crisis.

Is this book only about the U.S. financial system?

Yes, it focuses on the U.S., particularly the Federal Reserve and big financial institutions, but its lessons can apply globally.

What are some proposed solutions to avoid another doom loop?

Stricter regulations, transparency, and reducing reliance on government bailouts are key solutions discussed in the book.

Who would benefit most from reading this book?

Anyone interested in finance, economics, or understanding how big institutions shape our economy would find this book insightful.