“The End of Fractional Reserve Banking? Here’s What to Know”

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Is fractional reserve banking ending? Learn what it means, what’s changing, and how it impacts your money and the financial system today.

Introduction: What If the Rules of Money Just Changed?

For over a century, fractional reserve banking has been at the heart of how money flows through the economy. However, recent changes by central banks and shifts in how money is created have led some experts to ask: Is fractional reserve banking over? And if so, what does that mean for your savings, the economy, and the future of money?

In this guide, we’ll break it all down in simple terms—no PhD in economics is required. You’ll learn:

- What fractional reserve banking is (and isn’t)

- What’s changing in the banking system

- How it affects your personal finances

- And why it could signal a new era in monetary policy

Let’s dig into the real story behind the headlines—and what it means for you.

What Is Fractional Reserve Banking, Really?

➤ A Simple Definition

Fractional reserve banking is a system where banks are required to keep only a portion (or “fraction”) of their depositors’ money in reserve while lending out the rest. For example:

- You deposit $1,000.

- The bank keeps $100 (10% reserve) and lends out $900.

- That $900 ends up in someone else’s bank account, and the process repeats.

This system creates money through lending—and it’s one of the main ways the money supply grows in a modern economy.

➤ Why It Matters

Fractional reserve banking:

- Fuels economic growth by making loans more available.

- Increases the money supply through “money multiplication.”

- It introduces systemic risks like bank runs if too many people withdraw at once.

Has the Fed Already Ended Fractional Reserve Banking?

The Big Change: 0% Reserve Requirement

In March 2020, the Federal Reserve dropped the reserve requirement for banks to 0%. That means U.S. banks are no longer required to hold any portion of deposits in reserve.

Federal Reserve Announcement (March 2020)

Wait, So Does That Mean It’s Over?

Technically, yes. But here’s the nuance:

- Banks still manage reserves because of other regulations and liquidity needs.

- The Fed now controls lending behavior more through interest rates and capital requirements, not reserve mandates.

- The mechanism of money creation has shifted more towards central banks, especially through Quantitative Easing (QE).

⚠️ Controversial Question: Is Fractional Reserve Banking Still Used, or Is It Outdated?

Some economists argue that fractional reserve banking is misunderstood—or even obsolete.

Critics say:

- The focus on reserves is misleading.

- Modern banks create money by issuing loans and then find reserves afterward.

- Central banks backstop the entire system, so reserve ratios are symbolic.

This has fueled calls for:

- A move toward 100% reserve banking or

- A Sovereign Money System where only central banks can create new money.

Bank of England Report (2014): Money Creation in the Modern Economy

How This Affects You: Real-World Impacts

1. Savings Are Less Protected by Reserve Requirements

With 0% required reserves:

- Your bank might not hold any of your deposit as cash.

- However, FDIC insurance still protects deposits up to $250,000 per account.

2. Banks Rely on Central Bank Liquidity

- Instead of reserves, banks now rely more on Federal Reserve liquidity tools (like the discount window).

- In crises, this could centralize risk even more.

3. Money Creation Has Shifted Upstream

- The Fed creates digital money directly to support the financial system (as seen in QE programs).

- This blurs the line between central bank money and private bank-created money.

✅ Actionable Tips: How to Navigate the Changing System

1. Understand Where Your Bank Stands

Not all banks are equally exposed. Ask:

- Is your bank conservative with its lending practices?

- Does it hold excess reserves or rely on overnight borrowing?

2. Diversify Your Money Holdings

Spread your funds across:

- High-liquidity accounts

- FDIC-insured savings

- Treasury-backed options like I-Bonds or TreasuryDirect accounts

3. Stay Informed About Central Bank Policy

Watch for:

- Interest rate decisions

- Liquidity programs

- Moves toward Central Bank Digital Currencies (CBDCs)

Read our article: “CBDCs vs. Crypto – What’s the Real Digital Currency Revolution?”

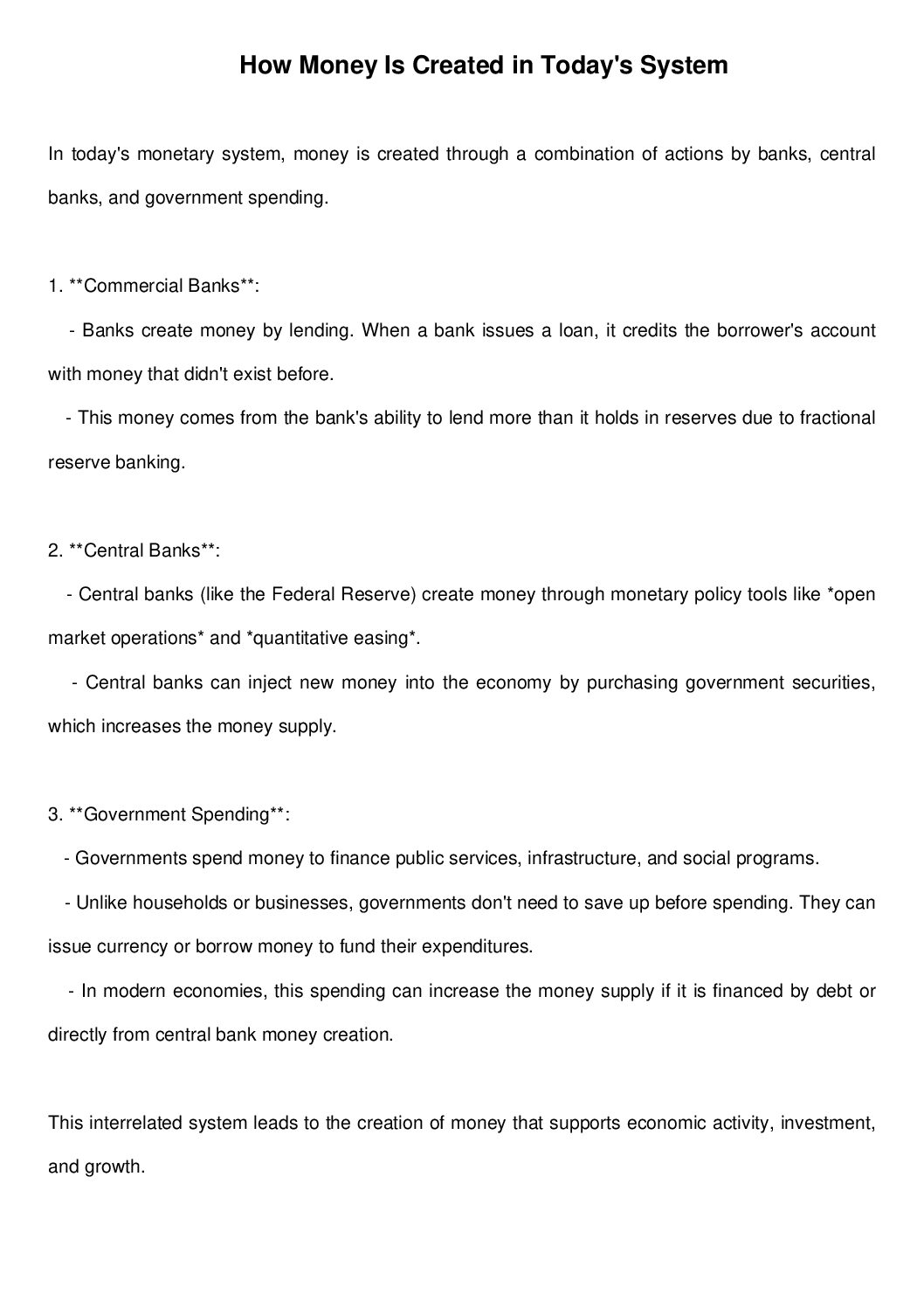

Get our downloadable PDF that shows how banks, central banks, and government spending create money in today’s system.

Free Download: “How Money is Really Created” – A Simple One-Page Visual Guide

{kind=link}

Related Articles from TheMoneyQuestion.org

- Modern Monetary Theory: Rethinking Economics and Monetary Reform

- Parasistem and the Sovereign Money System: What You Need to Know

FAQs: Fractional Reserve Banking Explained

- What does a 0% reserve requirement mean for everyday people?

Banks are no longer required to keep a specific amount of your deposit in reserve, but protections like FDIC insurance still apply.

- Is fractional reserve banking still in use?

Functionally, yes—but without mandated reserves, it operates more as a lending-first system guided by capital constraints.

- Does fractional reserve banking create money out of thin air?

In a way, yes. Banks create new money by issuing loans, expanding the total money supply.

- Could we switch to a 100% reserve system?

Yes, but it would be a major overhaul requiring new laws and structures, potentially slowing credit availability.

- Are central banks taking over money creation?

Increasingly, yes—especially through quantitative easing and potentially through digital currencies.

- Can banks lend more money than they have?

They can lend beyond deposits as long as they meet capital adequacy and liquidity requirements.

- What are the risks of eliminating reserve requirements?

Potential over-lending, centralization of risk, and greater dependence on central bank oversight.

- How can I protect my money in a changing system?

Diversify your holdings, understand bank stability, and monitor policy trends.

- Why did the Fed eliminate reserve requirements?

To provide more liquidity during COVID-19 and shift focus to more effective tools like interest rates.

- What’s the difference between reserves and capital?

Reserves are liquid funds held at the central bank. Capital is the bank’s own cushion against losses.

✅ Affiliate Disclosure

This post may contain affiliate links. If you click and make a purchase, TheMoneyQuestion.org may earn a small commission at no extra cost to you. We only recommend tools and resources we trust. Read our full disclosure here.

Leave a Reply