Bruce Creighton

Universal Basic Income: Pros, Cons, and Its Impact on the Economy

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Universal Basic Income: A Bold Economic Safety Net or a Costly Gamble?

Explore how Universal Basic Income could reduce poverty, spur entrepreneurship, and respond to automation — but face soaring costs, inflation risks, and political hurdles.

Introduction

Universal Basic Income is a revolutionary economic concept gaining traction worldwide. It proposes that every citizen receives a fixed, unconditional sum of money regularly, regardless of employment status. Proponents argue it could reduce poverty, simplify welfare systems, and adapt to automation-driven job losses. Critics warn of high costs, potential disincentives to work, and inflationary risks.

In this article, we’ll explore:

- What Universal Basic Income is and how it works

- The pros and cons of Universal Basic Income

- Its potential economic impact

- Real-world Universal Basic Income experiments and results

- FAQs and key takeaways

By the end, you’ll understand whether Universal Basic Income could be a viable solution for modern economies.

What Is Universal Basic Income (UBI)?

Universal Basic Income is a government-funded program that provides all citizens (or residents) regular, unconditional cash payments. Unlike traditional welfare, Universal Basic Income has no means-testing or work requirements. Key features include:

- Universal – Every eligible person receives it.

- Unconditional – No restrictions on how it’s spent.

- Regular – Typically distributed monthly.

How Would Universal Basic Income Be Funded?

Potential funding mechanisms include:

- Higher taxes (income, wealth, or VAT increases)

- Cutting existing welfare programs

- Printing money (risks inflation)

- Automation/AI taxes (on companies replacing workers with robots)

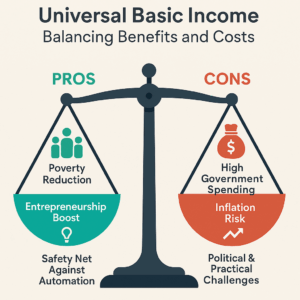

Pros of Universal Basic Income

- Poverty Reduction & Financial Security

- Provides a financial floor, reducing extreme poverty.

- Helps the unemployed, gig workers, and those in unstable jobs.

- Simplified Welfare System

- Replaces complex, bureaucratic welfare programs with direct cash transfers.

- Reduces administrative costs and fraud risks.

- Encourages Entrepreneurship & Creativity

- With basic needs covered, people may take risks (e.g., starting businesses, pursuing education, or starting creative ventures).

- Studies (e.g., Finland’s UBI trial) show improved mental health and well-being.

- Adaptation to Automation & Job Displacement

- As AI and robots replace jobs, UBI could act as a safety net.

- Prevents mass unemployment crises.

- Reduced Income Inequality

- Direct cash transfers help balance wealth distribution.

- Could decrease reliance on predatory loans and debt cycles.

Cons of Universal Basic Income

- High Cost & Funding Challenges

- A $1,000/month UBI for all U.S. adults would cost $3 trillion annually (nearly the entire federal budget).

- Requires major tax reforms or spending cuts.

- Potential Work Disincentives

- Critics argue free money could reduce motivation to work.

- Some studies (e.g., Alaska’s Permanent Fund Dividend) show minimal labour market impact, but long-term effects are unclear.

- Inflation Risk

- If demand surges (due to increased purchasing power), prices could rise, negating UBI’s benefits.

- It must be carefully balanced with monetary policy.

- Possible Reduction in Specialized Welfare

- Replacing targeted aid (e.g., disability, housing subsidies) with UBI might leave vulnerable groups worse off.

- Political & Public Resistance

- Many oppose “free money” on ideological grounds.

- Implementation requires bipartisan support, which is challenging.

Universal Basic Income’s Economic Impact

- Consumer Spending & Economic Growth

- More disposable income → higher consumption → economic stimulation.

- It could boost small businesses and local economies.

- Labor Market Effects

- Positive: Workers may seek better jobs rather than staying in exploitative roles.

- Negative: Some may exit the workforce, shrinking the labour supply.

- Government Budget & Taxation

- Requires massive fiscal restructuring.

- This could lead to higher taxes on corporations and high earners.

- Inflation & Monetary Policy

- If not properly managed, excess money supply could devalue the currency.

- Central banks may need to adjust interest rates accordingly.

Real-World Universal Basic Income Experiments

Several countries and cities have tested UBI with mixed results:

Experiment Findings

Finland (2017-2018) Improved well-being, no significant work disincentive.

Stockton, California (2019-2021) Reduced financial stress and increased full-time employment.

Kenya (Give Directly, ongoing) Boosted entrepreneurship and asset ownership.

Alaska (Permanent Fund Dividend since 1982) No major labour market disruption; popular but not a full UBI.

Most trials show positive short-term effects, but long-term sustainability remains uncertain.

Conclusion

In most serious political and economic proposals for a UBI, the model is not a full replacement for all welfare programs. The consensus among many UBI advocates is that the UBI would likely replace a large chunk of cash-transfer and income-support programs, but that highly-targeted benefits like disability assistance, specialized health care, and potentially housing support would need to be retained to avoid financially harming the most vulnerable citizens.

FAQs About Universal Basic Income

- Has any country fully adopted UBI?

As of late 2025, no country has fully implemented a nationwide UBI system that meets all the criteria (recurring, unconditional cash payments to all individual citizens). However, many countries and regions have explored the concept through:

- Pilot Programs and Trials (e.g. Finland, Canada, Kenya, various cities in the U.S. and Europe) to test the effects of a basic income on specific populations.

- Targeted Guaranteed Basic Income (GBI) programs for certain vulnerable groups, such as the one in Wales for young people leaving care.

- National cash Transfer programs that have some UBI-like features, such as Iran’s national cash transfer to all citizens that replaced subsidies (though this was a replacement for subsidies) or the Alaska Permanent Fund in the U.S., which gives annual dividends from oil revenues to all residents.

- Would UBI replace all welfare programs?

The idea of a UBI replacing all welfare programs is a central and highly debated point in the UBI discussion. There are two main philosophical models for how UBI would interact with existing welfare:

- The Replacement Model (“Big UBI), where UBI is set high enough to cover basic needs and would fully replace nearly all existing means-tested welfare programs (like unemployment insurance, food assistance, housing benefits and most cash transfers)

- The Complementary Model (The “Partial UBI” or UBI+) Here, UBI is set as a moderate, modest level (often below the poverty line) and would supplement the existing welfare system.

- How much would UBI cost taxpayers?

Estimates vary, but funding would likely require higher taxes on corporations, top earners, or new revenue streams. The cost of UBI to taxpayers is one of the most contentious points of the debate, and the answer is highly dependant on two key factors:

- The Gross Cost vs The Net Cost ( the biggest source of confusion)

- The Specific Design of the UBI (the payment amount and how it is funded)

- Would UBI cause inflation?

The consensus among economists is that UBI itself is not inherently inflationary or deflationary; its impact depends entirely on how it is funded and the current state of the economy. If not balanced with productivity growth, yes. Proper monetary policy would be crucial.

- Do people work less under UBI?

The overall effect on the labour market is generally small, but it does cause shifts in who works and why. Most experiments show no significant drop in employment, with some shifting to better jobs or education.

- Could UBI reduce homelessness?

Yes, UBI or targeted guaranteed income programs have shown promise in reducing housing instability and homelessness, particularly when paired with housing service. The core mechanism is addressing the income side of the housing crisis.

Homelessness is fundamentally a lack of housing, but it’s often caused by a lack of money. By providing an unconditional cash floor, UBI helps to stabilize people’s finances, allowing them to afford or save for housing.

- Is UBI socialist?

The question of whether UBI is socialist is complex, as UBI is a policy that is not confined to a single ideology and has been championed by thinkers from across the entire political spectrum. It’s debated—some see it as a market-friendly safety net, others as a redistribution policy.

- How would UBI affect gig workers?

UBI would likely have a profound and positive impact on gig workers by addressing the core issues of financial shortfalls, lack of benefits and low wages. It could provide stability for gig workers facing irregular income.

- Would UBI discourage education?

Unlikely, research and evidence from various pilot programs and studies on UBI suggest that it does not discourage education. In fact, many studies have shown the opposite: UBI can be a powerful tool to promote and support educational attainment and

skills training.

- What’s the biggest obstacle to UBI?

The biggest obstacle to implementing Universal Basic Income is not a single issue, but a combination of political, economic and social challenges. However, if one were to be identified as the most significant, it would be the immense cost and the resulting political feasibility of funding it.

Final Thoughts

Universal Basic Income presents a bold solution to modern economic challenges, from automation to inequality. While trials show promise, large-scale implementation remains complex. If balanced correctly, UBI could reshape economies—but without careful planning, it risks fiscal strain and unintended consequences.

For more on Universal Basic Income, check out the following:

Internal Link:

External Links:

- OECD: Basic Income Policy Option – 2017

- World Bank: Exploring Universal Basic Income

- KELA: Finland’s Basic Income Experiment 2017-2018

Disclosure

Affiliate Link Disclosure: TheMoneyQuestion.org may earn a small commission if you make a purchase through one of the links in this article. However, we only recommend products and services that we believe will add value to your financial journey.

Content Disclaimer: The information in this article is for informational purposes only and is not intended to substitute for the advice of a licensed or certified attorney, accountant, financial advisor, or other certified financial professionals. Always seek professional advice before making financial decisions.

Minimum Wage Increases: Do They Create Jobs or Cause Unemployment?

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Introduction

The debate over minimum wage increases is among the most contentious topics in economics and public policy. Proponents argue that raising the minimum wage boosts workers’ incomes, reduces poverty, and stimulates economic growth. Opponents, however, claim that higher wages lead to job losses, increased automation, and business closures.

In this article, we’ll examine the evidence on both sides, analyze real-world case studies, and explore whether minimum wage hikes create jobs or cause unemployment.

The Case for Minimum Wage Increases

- Minimum Wage Increases: Do They Create Jobs or Cause Unemployment?

Higher Earnings and Reduced Poverty

Studies show that increasing the minimum wage lifts workers out of poverty. According to a 2019 report by the Economic Policy Institute (EPI), a $15 minimum wage by 2025 would benefit over 32 million workers in the U.S.

A 2021 study published in the Quarterly Journal of Economics found that minimum wage increases significantly reduced poverty rates without causing substantial job losses.

- Increased Consumer Spending

Low-wage workers spend more of their income, leading to greater economic activity. The Federal Reserve Bank of Chicago found that a $1 minimum wage increase boosts household spending by about $700 per quarter.

- Lower Employee Turnover

Higher wages reduce turnover rates, saving businesses recruitment and training costs. A Harvard Business Review study found that companies paying above-market wages experienced 20% lower turnover.

- Job Creation Through Demand Growth

Some economists argue that higher wages increase demand for goods and services, leading to job growth. The Center for Economic and Policy Research (CEPR) suggests that modest wage hikes have neutral or slightly positive employment effects.

The Case Against Minimum Wage Increases

- Potential Job Losses

Classical economic theory suggests that artificially raising wages reduces employment opportunities. A 2014 Congressional Budget Office (CBO) report estimated that a $10.10 federal minimum wage could eliminate 500,000 jobs.

- Automation and Reduced Hiring

Businesses may replace workers with automation to offset higher labour costs. A National Bureau of Economic Research (NBER) study found that a $1 minimum wage increase leads to a 0.43% decline in low-skill employment due to automation.

- Small Business Struggles

Small businesses, particularly in low-margin industries like restaurants, may cut hours or shut down. A University of Washington study on Seattle’s $15 minimum wage found that hours worked by low-wage employees dropped by 6-7%.

- Regional Cost-of-Living Variations

A one-size-fits-all federal minimum wage may not account for regional economic differences. The American Enterprise Institute (AEI) argues that a $15 wage could devastate rural economies where living costs are lower.

Real-World Case Studies

- Seattle’s $15 Minimum Wage Experiment

Seattle’s phased minimum wage increase to $15 provided mixed results:

- Positive: Workers who kept jobs saw higher earnings.

- Negative: Some businesses reduced hiring, and low-skilled workers faced fewer opportunities.

- Germany’s National Minimum Wage (2015)

Germany introduced a €8.50 minimum wage in 2015. Studies by the German Institute for Economic Research (DIW) found:

- No significant job losses.

- Wage growth for low-income workers.

- UK’s National Living Wage

The UK’s gradual increases to a “National Living Wage” (currently £11.44 in 2024) showed:

- Increased earnings without significant unemployment spikes.

- There is some small business strain, but overall, economic resilience exists.

Conclusion: Do Minimum Wage Hikes Create or Kill Jobs?

The evidence supports the theory that moderate minimum wage increases (adjusted for inflation and regional costs) do not cause significant job losses but may lead to reduced hours or automation in some sectors. However, drastic hikes (like a sudden jump to $15 in low-cost areas) risk harming small businesses and low-skilled workers.

Policymakers should consider indexing wages to inflation, regional adjustments, and phased implementations to balance worker benefits with economic stability.

FAQs on Minimum Wage Increases

- Does raising the minimum wage always cause unemployment?

Not necessarily. Studies show modest increases often have minimal employment effects, but extreme hikes can lead to job cuts.

- How does the minimum wage affect small businesses?

Some small businesses may struggle with higher labour costs, leading to reduced hiring or price increases.

- Do higher wages lead to more automation?

Yes, some businesses invest in automation to offset rising labour costs.

- What is the “ripple effect” of minimum wage hikes?

Workers earning slightly above the new minimum may also demand raises, increasing overall wage growth.

- Does a higher minimum wage reduce poverty?

Yes, studies show it lifts many workers out of poverty, though some may lose hours or jobs.

- Why do some economists oppose minimum wage increases?

They argue it distorts labour markets, leading to job losses, especially for low-skilled workers.

- What’s the best way to implement a minimum wage increase?

Phased, regionally adjusted increases with inflation indexing are most effective.

- Has any country successfully implemented a high minimum wage?

Yes, countries like Australia and Germany have high minimum wages and strong employment rates.

- Do minimum wage hikes cause inflation?

They can contribute to localized inflation, but the overall impact is usually small.

- What are alternatives to minimum wage increases?

Alternative alternatives include expanding the Earned Income Tax Credit (EITC) or universal basic income (UBI).

Affiliate Marketing Disclosure

TheMoneyQuestion.org participates in affiliate marketing programs, meaning we may earn commissions on purchases made through our links. This helps support our research and content creation at no extra cost to you.

Final Thoughts

The minimum wage debate is complex, with valid arguments on both sides. While well-structured increases can improve living standards, policymakers must balance worker needs with economic realities.

What’s your take? Should the minimum wage be raised nationally, or should it vary by region? Let us know in the comments!

Who Pays For Bank Bailouts? The True Cost to Taxpayers and Consumers

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Who Pays For Bank Bailouts? The True Cost to Taxpayers and Consumers

Introduction

Bank bailouts are a contentious topic, often sparking debates about financial responsibility, economic stability, and fairness. When banks fail, governments frequently step in to prevent a broader financial crisis—but who ultimately foots the bill? The answer is usually taxpayers and consumers, either directly or indirectly.

In this post, we’ll explore:

- What bank bailouts are and why they happen

- The real cost to taxpayers and consumers

- Historical examples of major bailouts

- Alternatives to bailouts and their feasibility

- How bank bailouts impact everyday financial decisions

By the end, you’ll understand the hidden costs of bank bailouts and what they mean for your wallet.

What Is a Bank Bailout?

A bank bailout occurs when a government or financial institution provides financial support to a failing bank to prevent its collapse. This can take several forms:

- Direct cash injections (e.g., the U.S. Troubled Asset Relief Program, or TARP, in 2008)

- Government-backed loans at favourable rates

- Nationalization (where the government takes control of the bank)

- Debt guarantees (ensuring creditors won’t lose money)

Bailouts are typically justified as necessary to prevent economic contagion—where one bank’s failure triggers a chain reaction, leading to widespread financial instability.

Who Really Pays for Bank Bailouts?

While governments claim bailouts are a temporary measure, the costs are often passed down to:

- Taxpayers

Most bailouts are funded by public money, meaning taxpayers bear the burden. For example:

- The 2008 U.S. financial crisis saw $700 billion in taxpayer funds used to rescue banks.

- The UK’s bailout of RBS (Royal Bank of Scotland) cost taxpayers £45 billion.

Even when governments eventually recoup some funds (as with TARP), taxpayers still cover interest costs, administrative expenses, and losses from failed repayments.

- Consumers

Banks often raise fees, reduce interest on savings, or tighten lending to recover losses post-bailout. This means:

- Higher loan rates for mortgages and credit cards

- Lower savings yields (as banks prioritize profitability)

- Increased banking fees (e.g., overdraft charges)

- Future Generations

When governments borrow to fund bailouts, national debt increases, leading to:

- Higher future taxes

- Reduced public spending on infrastructure, healthcare, and education

Historical Examples of Bank Bailouts

- The 2008 Financial Crisis (U.S. & Global)

- TARP (Troubled Asset Relief Program): $700 billion in taxpayer funds used to stabilize banks, insurers (AIG), and automakers.

- UK’s Bailout of RBS and Lloyds: £137 billion spent to prevent systemic collapse.

- The Savings and Loan Crisis (1980s-1990s, U.S.)

- Cost taxpayers $124 billion.

- European Debt Crisis (2010s)

- Ireland’s bailout of Anglo-Irish Bank: Cost €29.3 billion, leading to years of austerity.

Are There Alternatives to Bank Bailouts?

Instead of taxpayer-funded rescues, some propose:

- Bail-Ins

- Banks use their own assets or convert debt to equity rather than relying on public funds.

- Example: In Cyprus’s 2013 crisis, depositors with over €100,000 took losses.

- Stronger Regulation & Capital Requirements

- Higher reserve ratios to ensure banks can withstand shocks.

- Stress tests to identify vulnerabilities early.

- Letting Banks Fail (Market Discipline)

- Moral hazard (banks taking excessive risks knowing they’ll be bailed out) could be reduced.

- Example: Lehman Brothers’ 2008 collapse—though chaotic, it forced reforms.

How Bank Bailouts Affect You

Even if you don’t work in finance, bailouts impact:

- Your taxes (funding bailouts means less money for public services).

- Your savings and loans (banks may offer worse rates to recoup losses).

- Economic inequality (bailouts often benefit wealthy investors over ordinary citizens).

Conclusion: Who Really Bears the Cost?

Bank bailouts are sold as necessary to prevent economic disaster, but the true cost falls on taxpayers and consumers. While some argue they’re unavoidable, alternatives like bail-ins, stricter regulations, and market discipline could reduce reliance on public funds.

The next time a bank fails, ask: Should taxpayers pay, or should the financial sector bear its own risks?

FAQs About Bank Bailouts

- Do taxpayers always pay for bank bailouts?

Mostly yes—either directly (via government funds) or indirectly (through higher banking costs).

- Have any banks repaid bailout money?

Some have (e.g., U.S. banks repaid TARP funds with interest), but many bailouts result in net losses.

- What’s the difference between a bailout and a bail-in?

A bailout uses public money; a bail-in forces banks to use their own funds or impose losses on creditors.

- Why can’t we just let banks fail?

Fear of systemic collapse—but some argue short-term pain could lead to long-term stability.

- Do bailouts encourage reckless banking?

Yes, via moral hazard—banks may take bigger risks knowing they’ll be rescued.

- Which was the most expensive bailout in history?

The 2008 U.S. financial crisis, with $700 billion in TARP funds plus trillions in Fed support.

- How do bailouts affect inflation?

If governments print money to fund bailouts, it can devalue currency and fuel inflation.

- Are credit unions and small banks bailed out too?

Rarely—most bailouts focus on “too big to fail” institutions.

- Can individuals claim compensation from bailouts?

No—taxpayers bear costs without direct reimbursement.

- What can I do to protect my money from bailout risks?

- Diversify savings (use credit unions, ETFs, or non-bank investments).

- Support financial reform (advocate for stricter banking regulations).

Disclosure & Affiliate Note

Disclosure: This post may contain affiliate links. If you make a purchase through these links, we may earn a commission at no extra cost to you. We only recommend products/services we believe in.

Tariffs: A Comprehensive Guide to How They Work and Who Ultimately Pays

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Introduction

Tariffs have been a hot topic in global trade discussions for centuries. Understanding tariffs is crucial whether you own a business, a consumer, or someone interested in economics. They influence the prices of goods, impact international relations, and can even shape entire economies. But what exactly are tariffs, how do they work, and who ultimately pays for them? This guide will explain everything you need to know about tariffs, their implications, and their real-world effects.

What Are Tariffs?

Tariffs are taxes imposed by a government on imported goods and services. They are designed to achieve several objectives, such as protecting domestic industries, generating revenue, or retaliating against trade practices deemed unfair. Tariffs can be determined as specific (a fixed fee per unit) or ad valorem (a percentage of the item’s value).

How Do Tariffs Work?

- Imposition: A government decides to impose a tariff on specific goods. For example, the U.S. might impose a 25% tariff on steel imports from China.

- Collection: When the goods arrive at the border, the importer must pay the tariff to the customs authority.

- Impact: The cost of imported goods increases, leading to higher consumer prices, changes in supply chains, or shifts in trade patterns.

Types of Tariffs

- Protective Tariffs: Aimed at shielding domestic industries from foreign competitors by making imported goods more expensive.

- Revenue Tariffs: Designed primarily to generate income for the government.

- Retaliatory Tariffs: Imposed in response to another country’s trade policies, often as a form of economic sanction.

The Economic Impact of Tariffs

On Domestic Industries

Tariffs can give domestic producers a competitive edge by making imported goods more expensive. This can lead to increased production, higher employment, and more significant investment in local industries. However, reduced competition can also lead to inefficiencies and a lack of innovation.

On Consumers

Consumers often bear the brunt of tariffs through higher prices. For example, if a tariff is imposed on imported electronics, the cost of smartphones, laptops, and other gadgets may rise. This can reduce purchasing power and overall consumer welfare.

On International Trade

Tariffs can lead to trade wars, where countries retaliate with their tariffs or use them as a negotiation tool to obtain non-trade concessions. This can disrupt global supply chains, reduce international trade volumes, and lead to economic instability. For instance, the U.S.-China trade war saw both countries imposing tariffs on billions of dollars worth of goods, affecting global markets.

Who Ultimately Pays for Tariffs?

While importers technically pay tariffs, the cost is often passed down the supply chain, ultimately landing on consumers. Businesses may absorb some of the costs initially, but to maintain profit margins, they typically raise prices. In some cases, tariffs can also lead to job losses in industries that rely on imported materials.

Case Studies

- The Smoot-Hawley Tariff Act (1930): This U.S. legislation raised tariffs on over 20,000 imported goods, significantly decreasing international trade and exacerbating the Great Depression.

- U.S.-China Trade War (2018-present): Tariff impositions have increased costs for businesses and consumers in both countries, disrupting supply chains and creating economic uncertainty.

Conclusion

Tariffs are a complex and multifaceted tool in international trade. While they can protect domestic industries and generate revenue, they also have significant downsides, including higher consumer prices and potential trade wars. Understanding how tariffs work and their broader economic impact is necessary for making informed decisions, whether you’re a business owner, consumer, or investor.

By understanding the intricacies of tariffs, you can make better decisions to navigate the complexities of global trade, resulting in more informed economic choices. Stay tuned to TheMoneyQuestion.org for more insights and analysis on critical financial topics.

Disclosure Note

This post may contain affiliate links. If you click on an affiliate link and purchase, we may receive a small commission at no extra cost. This helps support our work and allows us to continue providing valuable content. Thank you for your support!

Your Go-To Guide for Virtual Wealth System Resources

| Platform | Best For | Pricing | Perks |

| Shopify | Online stores | From $39/month | Easy setup for e-commerce. |

| Wealthfront | Automated investing | 0.25% annual fee | Hands-off and low-cost. |

| ClickFunnels | Sales funnels | From $127/month | Great for boosting sales. |

| Robinhood | Stock trading | Free, premium optional | Beginner-friendly with no hidden fees. |

| Zapier | Task automation | Free, paid from $20/mo | Connects apps and saves time. |

Key Takeaway: Virtual wealth systems offer tools to help you grow and manage your finances digitally. The right resources can boost your results and simplify your journey.

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

What Exactly Are Virtual Wealth Systems?

- Virtual wealth systems: These are digital platforms designed to help you build and manage wealth online. They cover everything from investing and trading to affiliate marketing and e-commerce. These systems bring together automation, analytics, and educational tools to save you time and energy.

- Why use them: They help streamline tasks and amplify results. Automation handles repetitive work, scalability allows you to grow without burning out, and accessibility lets you operate from anywhere with an internet connection.

- Popular platforms: Shopify for e-commerce, Wealthfront for investments, and ClickFunnels for affiliate marketing are just a few examples of the many options available.

Must-Have Resources for Virtual Wealth Success

- Learning tools: You can’t succeed without understanding the basics. Luckily, there are tons of resources out there, from online courses to blogs. Platforms like Udemy and Coursera are perfect for learning the ropes, while blogs like NerdWallet keep you updated on trends.

- Tools and software: Having the right tech can make all the difference. Automation tools like Zapier and HubSpot can take care of repetitive tasks, while analytics platforms like Google Analytics and SEMrush help track performance and uncover growth opportunities.

- Communities and networking: Connections can be just as valuable as tools. Joining forums like Reddit’s r/Entrepreneur or LinkedIn groups can give you access to advice, ideas, and even potential partnerships.

Financial Tools You Shouldn’t Miss

- Budgeting apps: Want to stay on top of your spending? Apps like Mint and YNAB (You Need a Budget) are lifesavers. They keep track of your expenses and help you stick to your financial goals.

- Investment platforms: Platforms like Robinhood, E*TRADE, or Acorns make it easy to grow your wealth. They cater to everyone, whether you’re a beginner or a pro, with tools like automated portfolios and live market updates.

- Tax management software: Taxes don’t have to be stressful. With tools like TurboTax and QuickBooks, you can simplify the process and stay on top of your responsibilities.

How to Make the Most of Virtual Wealth Resources

- Pick tools that match your goals: Look for platforms that fit what you want to achieve, whether that’s growing passive income or building an online store.

- Keep learning: Trends and strategies change, so it’s important to stay informed by reading blogs, attending webinars, or watching tutorials.

- Diversify: Don’t put all your eggs in one basket. Spread out your efforts to reduce risks and maximize potential gains.

Key Takeaway: The more you understand and adapt, the better you’ll be at navigating and succeeding in the digital wealth space.

Overcoming Common Challenges

- Feeling overwhelmed: It’s easy to feel lost with so many options out there.

- Solution: Start with platforms that align with your current goals and build from there.

- Managing your time: Balancing multiple tasks can be tricky.

- Solution: Use time-tracking apps like Toggl to stay organized.

- Staying consistent: Sometimes, progress feels slow.

- Solution: Set small milestones and celebrate when you reach them—it helps keep the momentum going.

Wrapping It Up

Virtual wealth systems are an amazing way to take control of your financial future. With the right mix of tools, strategies, and effort, you can grow your wealth while keeping things simple. Start small, stay consistent, and keep learning. Before you know it, you’ll be well on your way to success.

FAQs

What’s the best way to start with virtual wealth systems?

Start with a platform that fits your goals, like Shopify for e-commerce or Robinhood for investments. Explore their features and take advantage of tutorials.

Are virtual wealth systems beginner-friendly?

Absolutely! Many platforms have beginner-friendly versions and guides to help you get started.

Do I need to spend a lot of money upfront?

Not necessarily. Many tools offer free versions, and you can upgrade as you grow.

How can I avoid scams?

Stick to well-reviewed platforms and do thorough research before committing to anything.

Can I succeed with just one platform?

Yes, but diversifying your efforts across multiple platforms can help you grow faster and reduce risks.

Understanding Money 101: Your Guide to Managing Finances with Confidence

| Savings Option | Interest Rate | Access | Risk | Best For |

| Regular Savings | Low | Anytime | Very low | Daily use, emergencies |

| High-Yield Savings | Higher | Online, easy | Very low | Faster growth |

| CDs | High | Locked-in | Very low | Long-term savings |

| Money Market | Moderate | Limited withdrawals | Very low | Flexible savings + growth |

What is Money Anyway?

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Money isn’t just coins, cash, or numbers on a screen. It’s a tool we use to trade goods and services, measure value, and store wealth. Over the years, it has evolved from bartering to physical currencies and, more recently, to digital forms like cryptocurrencies.

Takeaway: When you understand how money works, you can make smarter decisions about using it.

The Different Kinds of Money

- Good Old Physical Money: Cash and coins might seem old-school, but they’re still super important, especially in places where digital payments aren’t as common.

- Digital Money for the Win: Think credit cards, apps, or even Bitcoin. Digital money makes life easier and faster but needs a little extra care to avoid overspending.

- Value Beyond the Dollar: Stocks, bonds, and gold aren’t cash, but they’re valuable assets that can help grow your wealth over time.

Takeaway: Having a mix of physical, digital, and investment-based money gives you more financial security.

Earning Money: Start Where You Are

We all want more money coming in, right? Whether it’s from a job, a business, or a side hustle, earning is the foundation of financial success.

- The Classic Paycheck: Your regular job is often the main source of income. Build your skills and take advantage of opportunities to grow.

- Think Outside the Box: Freelancing, renting out a property, or selling products online can be great ways to bring in extra cash.

Takeaway: Don’t rely on one income stream—having options gives you more stability and freedom.

Saving Money: Build Your Safety Net

Saving isn’t just for emergencies—it’s about giving your future self some breathing room.

- Set Up an Emergency Fund: Aim to save enough to cover 3-6 months of expenses. This is your safety cushion for when life throws a curveball.

- Make Saving Automatic: Saving gets easier when it’s automatic. Set up transfers to your savings account, and let it grow without the hassle.

Takeaway: Saving now means less stress later, plain and simple.

Budgeting Basics: Where’s Your Money Going?

A budget is your financial GPS—it shows you where your money is going and helps you stay on track.

- Try the 50/30/20 Rule: Split your income into 50% for needs, 30% for wants, and 20% for savings or debt payments. Simple and effective.

- Zero-Based Budgeting: Every dollar gets a job. Whether it’s for bills, groceries, or fun, assign it a purpose so nothing goes to waste.

- Use Budgeting Apps: Apps like Mint or YNAB (You Need a Budget) can make managing your money way easier.

Takeaway: When you’re in control of your budget, you’re in control of your money.

Spending Wisely: Shop Smarter, Not Harder

Spending money isn’t bad, but doing it without a plan can cause problems.

- Needs vs. Wants: Take a second to think: Do you need it, or do you just want it? Knowing the difference is a game-changer.

- Plan for Big Purchases: Saving up for big-ticket items helps you avoid debt and feel good about spending.

- Look for Deals: Why pay full price when you can save? Use discounts, cashback programs, or sales to stretch your dollars further.

Takeaway: Spending intentionally means you’ll have more money for the things that really matter.

Understanding Debt: Handle It Like a Pro

Debt can be tricky, but not all debt is bad. The key is managing it wisely.

- The Good vs. the Bad: Good debt, such as a mortgage or student loans, can set you up for a stronger future. Bad debt, like high-interest credit cards, can keep you trapped.

- How to Pay It Off:

- Snowball Method: Start small and work your way up. Paying off smaller debts first keeps you motivated.

- Avalanche Method: Attack the debt with the highest interest rate first to save more money in the long run.

Takeaway: Stay on top of your debt so it doesn’t stay on top of you.

Investing: Your Money, Working for You

Investing might sound intimidating, but it’s really about making your money grow.

- Start Small: Begin with low-risk options like index funds or bonds. You’ll learn the ropes while keeping risks low.

- Risk vs. Reward: The bigger the potential reward, the bigger the risk. Be sure to balance risky investments with safer ones.

- Think Long-Term: Investing is a long-term game. The sooner you start, the more you’ll benefit from compound interest down the road.

Takeaway: Even small investments now can lead to big results later.

Money Tips for Every Stage of Life

Your financial needs change as you grow, and so should your money habits.

- In Your 20s and 30s: Learn the basics, start saving, and invest in building your career.

- Building a Family: Plan for major expenses like a home, education, and healthcare. Balance saving and spending carefully.

- Retirement Years: Shift your focus to generating steady income and protecting your savings.

Takeaway: Tailor your money strategies to fit where you are in life.

Staying Informed: Keep Learning

- Follow Trends: Stay updated on market changes, interest rates, and economic news that might affect your finances.

- Read and Listen: Books, podcasts, and financial blogs are great for learning new strategies and staying inspired.

- Ask for Help: Financial advisors can give you tailored advice to help you reach your goals more quickly.

Takeaway: The more you know, the better your money moves will be.

Conclusion

Managing money doesn’t have to be hard. When you understand how it works, set a budget, save, and invest, you’re on the right track. Even small actions add up over time.

FAQs

How do I decide if I should save or invest?

If you don’t have an emergency fund, save first. Once that’s covered, start investing for long-term growth.

What’s the biggest mistake people make with credit cards?

Overspending and not paying the balance in full each month. Interest can pile up quickly if you’re not careful.

How do I teach my kids about money?

Start small with lessons about saving, like using a piggy bank. As they grow, involve them in simple budgeting and spending decisions.

The Pandemic’s Financial Maze: Insights from The Doom Loop

| Aspect | 2008 Crisis | Pandemic Crisis |

| Focus | Banks and mortgages | Economy, jobs, businesses |

| Interest Rates | Gradual cuts | Immediate drop to near-zero |

| Quantitative Easing | Stabilized banks | Broad liquidity injection |

| Bailouts | Banks and automakers | Businesses, states, cities |

| Programs | TARP | PPP, direct loans |

| Outcome | Slow recovery | Quick response, long risks |

The Economy in Chaos: How the Pandemic Started It All

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

When the pandemic hit, it felt like the economy slammed into a brick wall. Businesses shut down, people lost jobs, and everything seemed uncertain. That’s when the Federal Reserve stepped in to prevent an all-out collapse.

- What Did the Fed Do?: The Fed pulled out all the stops to keep things afloat. Interest rates were slashed to nearly zero, making borrowing money cheaper. They introduced quantitative easing (QE), where the Fed started buying assets to pump money into the system and prevent market freezes. Emergency loan programs were also rolled out to help businesses, cities, and financial institutions stay afloat.

- Big Finance’s Role: Big banks and investment firms were key players during this time. They helped stabilize things by distributing loans and offering financial support. But they also added fuel to the fire by relying on risky investments, making the financial system even more fragile.

What’s the Doom Loop All About?

The “doom loop” is the star of the book. It’s a vicious cycle where financial instability forces interventions like bailouts or QE, which then create even more risks down the line.

Low interest rates encourage banks and firms to take on more risk because borrowing is so cheap. A handful of big players controlling massive chunks of the market makes the system fragile. Financial institutions start expecting help whenever things go south, leading to risky behavior and a dependency on government interventions.

Takeaway: The doom loop shows how quick fixes can sometimes make long-term problems worse.

What the Book Does Well

There’s a lot to love about The Doom Loop. It’s well-researched, insightful, and explains tricky concepts in a way that doesn’t feel like a college textbook.

- Complex Topics Made Simple: The authors break down complicated financial policies into something even non-experts can understand. If you’ve ever wondered how QE or bailouts actually work, this book explains it clearly.

- Fair Critique of the Fed: Instead of just bashing the Federal Reserve, the book offers a balanced take. It gives credit where it’s due while pointing out areas where the Fed might’ve dropped the ball.

- Behind the Scenes of Big Finance: The book takes you into the world of big banks and investment firms, showing how their strategies can both stabilize and destabilize the economy.

Where the Book Could Do Better

No book is perfect, and The Doom Loop has a couple of areas where it could have gone further.

- A Little Too Technical at Times: Some parts lean heavily on financial jargon, which could make casual readers feel a bit lost.

- It’s All About the U.S.: While the focus on the U.S. financial system is understandable, it would’ve been great to see more comparisons with how other countries handled the pandemic.

Why It Matters Today

This book isn’t just a recap of what happened; it’s a warning and a guide for what we should watch out for in the future.

- Fixing the System: One big takeaway is that we need better regulations to keep the financial system stable. That means things like stricter rules on how much risk banks can take and more transparency about their practices.

- Breaking the Cycle: The dependency on government bailouts and interventions has created what’s known as a moral hazard. Financial institutions take risks because they expect to be rescued if things go wrong. That needs to change.

- Preparing for the Next Crisis: The pandemic taught us a lot about how fragile our systems are. By learning from what worked—and what didn’t—we can be better prepared for whatever comes next.

Takeaway: The lessons from this book aren’t just for economists or policymakers. They’re for anyone who wants to understand how financial systems impact all of us.

Wrapping It Up

The Doom Loop: The Fed and Big Finance in the Pandemic is an eye-opening look at how the financial world responded to one of the biggest crises of our time. It doesn’t shy away from tough questions and leaves readers with plenty to think about. If you’re curious about how monetary policy and big finance shape the world we live in, this book is a must-read.

FAQs

What exactly is the doom loop?

It’s a cycle where financial instability forces interventions like bailouts, which end up creating even more risks, leading to more instability.

How did the pandemic affect small businesses financially?

The Federal Reserve’s actions, like providing emergency loans and lowering interest rates, helped small businesses access funds to stay afloat during the crisis.

Is this book only about the U.S. financial system?

Yes, it focuses on the U.S., particularly the Federal Reserve and big financial institutions, but its lessons can apply globally.

What are some proposed solutions to avoid another doom loop?

Stricter regulations, transparency, and reducing reliance on government bailouts are key solutions discussed in the book.

Who would benefit most from reading this book?

Anyone interested in finance, economics, or understanding how big institutions shape our economy would find this book insightful.

Special Purpose Money: A Game-Changer for Limited Globalization

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

| Type | Purpose |

| Localized Currencies | Boosts local trade and supports communities. |

| Industry Tokens | Simplifies transactions in specific sectors. |

| Carbon Credits | Aids in meeting environmental goals. |

| Healthcare Vouchers | Allocates funds for medical services. |

| Digital Government Money | Ensures secure and efficient transactions. |

What Exactly is Special Purpose Money?

Special purpose money is like the Swiss Army knife of currencies—it’s designed for specific uses rather than being a one-size-fits-all solution like traditional money. Whether it’s tied to a particular industry, region, or transaction type, SPM is tailored to get the job done.

- What makes it special: It’s not meant to replace traditional money but rather to enhance it in targeted ways. SPM focuses on efficiency and solving specific financial problems.

- How it’s designed: SPM often incorporates advanced technology like blockchain, which enables things like smart contracts or restricted spending for predefined purposes.

- Why it’s important: As economies prioritize regional trade, SPM ensures that financial systems evolve to meet these specific needs effectively.

Why Do We Need It in Limited Globalization?

Limited globalization is all about balancing global connectivity with local focus. As countries look inward to boost local economies, SPM becomes a natural fit.

- Supports local trade: SPM ensures that money stays within regional economies, helping local businesses thrive.

- Reduces global currency dependency: It minimizes reliance on major currencies like the USD or Euro, which can be volatile.

- Simplifies trade processes: Whether it’s industry-specific or community-focused, SPM makes transactions smoother and more reliable.

Quick Takeaway: As the world shifts toward localized economies, SPM offers the perfect solution to balance autonomy and trade.

What Can Special Purpose Money Do?

- Boost local trade: Imagine a currency created just for a farming community or a local business hub. It helps keep money circulating within the community and strengthens the local economy.

- Reduce risk from currency fluctuations: Global currencies can be unpredictable. SPM shields local economies from these ups and downs, creating a more stable financial environment.

- Encourage economic independence: SPM empowers countries and regions to make their own financial rules, tailoring money to fit their unique needs.

How Does Special Purpose Money Work in Real Life?

- Localized currencies: Think about the Bristol Pound in the UK or BerkShares in the U.S. These local currencies keep money within the community, helping local businesses thrive.

- Industry-specific tokens: SPM can be tailored for particular industries, like energy credits or carbon offset tokens. For instance, healthcare vouchers can ensure funds are allocated exactly where they’re needed.

- Government-led initiatives: Some countries are exploring digital currencies issued by their central banks. These digital currencies aim to make transactions faster and more secure while supporting local economies.

Why Special Purpose Money is Worth Considering

- It’s efficient: SPM speeds up transactions by cutting out middlemen. Technologies like blockchain can automate processes, making everything faster and smoother.

- It promotes stability: By isolating local economies from the unpredictability of global markets, SPM provides a sense of financial security.

- It inspires innovation: SPM isn’t just about money—it’s driving advancements in technology and finance, opening doors for industries far beyond banking.

Quick Takeaway: SPM is more than a financial tool—it’s a driver for technological and economic growth.

What Are the Challenges?

- Getting people on board: Change is hard, and many people are hesitant to move away from the financial systems they know. Education and clear benefits are key to overcoming this.

- Navigating rules and regulations: Creating and using SPM means dealing with a lot of legal and regulatory hurdles. It’s not impossible, but it’s definitely something to keep in mind.

- Scaling it up: SPM works great in specific cases, but expanding it to broader markets requires a lot of investment in technology and infrastructure.

What’s Next for Special Purpose Money?

- A tech-driven future: With innovations in blockchain and AI, SPM will only get smarter, more secure, and easier to use.

- Expanding its reach: While it’s currently focused on niche markets, SPM has the potential to bridge local economies with global trade networks.

- Supporting sustainability: SPM could also play a big role in promoting environmentally friendly practices, making it a win-win for the economy and the planet.

Quick Takeaway: The future of SPM lies in combining cutting-edge tech with sustainable practices to create a balanced financial system.

Wrapping It Up

Special purpose money is changing the game for economies shifting toward limited globalization. By supporting local trade, reducing reliance on volatile global currencies, and promoting innovation, it’s paving the way for a new kind of financial system. The potential is huge, and as more industries and regions adopt SPM, it’s set to become a key player in the evolving global economy.

FAQs

What sets special purpose money apart from traditional currencies?

SPM is designed for specific uses, like regional trade or industry-focused transactions, while traditional currencies are more generalized.

Do we need blockchain for special purpose money to work?

Not necessarily. While blockchain makes SPM more efficient, other digital systems can also support it.

Which industries are best suited for special purpose money?

Industries like agriculture, healthcare, and energy are prime candidates for SPM due to their need for precise and efficient transaction systems.

Are there risks with adopting special purpose money?

Yes, there are challenges like regulatory issues, adoption hesitancy, and technological limitations. However, these can be managed with the right strategies.

Will special purpose money replace traditional currencies?

No, SPM is meant to complement traditional currencies by addressing specific needs, not to replace them entirely.

Sir Ben Marx: From Monetary Theory to Financialization

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

| Aspect | Monetary Theory | Financialization |

| Focus | Money stability. | Growth of financial markets. |

| Purpose | Economic stability. | Maximizing financial returns. |

| Key Players | Central banks, governments. | Banks, markets, investors. |

| Impact | Steady growth. | Rapid gains, higher risks. |

| Wealth | Balances distribution. | Widens inequality. |

| Criticism | Slow to adapt. | Overfocus on speculation. |

Who Was Sir Ben Marx?

Sir Ben Marx was an economist whose innovative ideas connected traditional monetary theory with the complexities of modern financial systems. His work didn’t just influence academics—it shaped real-world policies and provided a framework for understanding today’s global financial landscape. By combining deep theoretical knowledge with practical solutions, Marx became a pioneer in bridging the gap between monetary principles and financial markets.

What Did Marx Say About Money?

Marx’s monetary theory revolved around the role of money as a stabilizing force in economies. He believed that for an economy to thrive, there needed to be a balance in how money is supplied and circulated. Key insights from his work include:

- Balancing Money Supply: Marx argued that inflation and deflation could be controlled by maintaining the right amount of money in circulation.

- Trust in Monetary Systems: He emphasized that public confidence in money is vital for a stable economy. Without trust, even the most robust monetary systems can crumble.

- Behavioral Economics: Marx explored how psychological factors, like spending habits and public sentiment, impact the effectiveness of monetary policies.

Marx also advocated for adapting monetary systems to align with technological advancements, including the potential for digital currencies.

What Is Financialization?

Financialization refers to the growing dominance of financial markets and institutions in shaping economies. It’s a shift from traditional sectors like manufacturing and agriculture to a focus on financial instruments and markets. Marx was ahead of his time in recognizing this trend and its implications.

- Shifting Wealth: Financialization moves wealth from physical goods to intangible financial assets.

- Debt Dependency: While debt can fuel growth, Marx warned of the risks of excessive borrowing, which could lead to economic instability.

- Widening Wealth Gaps: Financialization often benefits the wealthy, exacerbating income inequality and creating economic divides.

Marx acknowledged the efficiency financialization brought but was vocal about the risks if left unchecked.

Why Marx’s Work Still Matters

Sir Ben Marx’s theories continue to guide policymakers and economists worldwide. His focus on monetary stability remains relevant as central banks and governments navigate inflation, financial crises, and currency regulation. Beyond academia, Marx’s work is a practical tool for tackling the challenges of today’s globalized financial systems.

In educational institutions, his theories are integral to understanding how monetary policies interact with financial markets. Students and professionals alike draw from his work to address modern economic complexities.

Critiques of Marx’s Ideas

Even though Marx’s ideas are widely celebrated, they have faced criticism over time. Here are some common points of contention:

- Adapting to Technology: Critics argue that Marx’s theories need updating to address innovations like cryptocurrency and blockchain technology.

- Applicability to Emerging Markets: His work largely focused on developed economies, leaving questions about its relevance in developing regions.

- Regulation vs. Innovation: Marx’s emphasis on regulation has sparked debate about whether it limits economic creativity and growth.

Despite these critiques, his ideas remain foundational for understanding the dynamics between money and markets.

Key Takeaway: Sir Ben Marx’s legacy lies in his ability to connect monetary theory with the realities of financialization. His insights offer a guide for navigating economic challenges by focusing on stability, adaptability, and the role of public trust.

FAQs

What is financialization, and why is it important?

Financialization is the increased role of financial markets in the economy. It matters because it shifts wealth creation and distribution, often prioritizing financial instruments over traditional industries.

How does public trust affect monetary systems?

Public trust is crucial for monetary stability. If people lose confidence in the value of money, it can destabilize the entire economy.

What risks did Marx identify with financialization?

Marx warned about risks like over-reliance on debt, widening wealth inequality, and economic instability caused by focusing too heavily on financial markets.

Are Marx’s ideas relevant to digital currencies?

Yes, Marx’s emphasis on monetary stability and adaptability makes his theories applicable to the integration of digital currencies into modern economies.

How did Marx influence modern economic policies?

His theories have shaped how governments and central banks manage inflation, regulate financial markets, and maintain currency stability.

Parasistem and the Sovereign Money System: What You Need to Know

| Benefit | How It Helps |

| Efficiency | Speeds up transactions and simplifies processes. |

| Security | Adds protection with blockchain to reduce fraud risks. |

| Trust | Ensures transparency in money flow and decisions. |

| Inclusion | Makes systems accessible to underbanked communities. |

| Scalability | Adapts easily to growing financial demands. |

What Is Parasistem?

- Understanding parasistem: At its core, parasistem is a supportive system that enhances the operations of primary monetary frameworks like the sovereign money system. Imagine a sidekick that works alongside the main financial system to fill in gaps, improve efficiency, and boost accessibility. That’s parasistem in action.

- Decentralization at its heart: Parasistem is all about decentralization. Instead of relying on a central authority like traditional systems, it uses cutting-edge technology to run smoothly. It’s flexible, forward-thinking, and built to evolve with global economic shifts, making it a key player in connecting centralized and decentralized finance.

- A broader perspective: Parasistem isn’t limited to one definition. Its applications and benefits vary depending on the context. Whether it’s enhancing financial inclusion or streamlining transactions, parasistem’s value lies in its versatility.

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

A Quick Look at the Sovereign Money System

- What is a sovereign money system? It’s a monetary framework where a nation’s central authority—like a national bank—is in charge of issuing currency. It eliminates reliance on commercial banks to create money, offering more stability and transparency.

- Core principles of sovereign money: The system is built on three main ideas. First, it centralizes control over money, reducing risks from private institutions. Second, it uses fiat currency, which gets its value from government backing. Finally, it emphasizes accountability, ensuring that citizens can trust the system.

- Why it matters: This setup keeps inflation in check, prevents economic instability, and creates a financial foundation that everyone can rely on.

How Parasistem Fits Into Sovereign Money Systems

- Bridging gaps: Parasistem complements sovereign money systems by addressing their limitations. While the latter ensures stability and centralized control, parasistem introduces decentralized elements, creating a balanced and adaptable framework.

- Driving inclusivity: One of parasistem’s most impactful roles is in financial inclusion. By leveraging decentralized technologies, it reaches underbanked populations, providing them access to essential financial services.

- Making systems flexible: Parasistem adapts to the ever-changing financial landscape. It adds a layer of innovation that allows sovereign money systems to evolve without compromising their core principles.

- Boosting performance: Through advanced technology, parasistem enhances operational efficiency, ensuring smoother and faster transactions. Its ability to scale with demand makes it indispensable in modern economies.

What Makes Parasistem So Beneficial?

- Efficiency and speed: Parasistem integrates advanced technologies to streamline processes, making financial transactions faster and more reliable. Its efficiency helps reduce bottlenecks, saving time and resources.

- Enhanced security: By incorporating blockchain and other cutting-edge tools, parasistem adds a robust layer of security. This minimizes the risks of fraud, cyberattacks, and data breaches, ensuring safer financial systems.

- Transparency builds trust: Parasistem fosters trust by ensuring transparency in financial operations. Users can monitor how money flows and how decisions are made, creating confidence in the system.

- Inclusivity and accessibility: Parasistem shines in making financial systems accessible to underserved communities. By connecting traditional banking with remote areas, it helps ensure everyone gets included.

- Adaptability: As financial demands grow, parasistem can scale effortlessly. Its adaptability ensures that systems remain efficient and effective, even in the face of increasing pressures.

The Challenges That Come With Parasistem

- Regulatory issues: Combining decentralized features with centralized systems is complex. Governments must create clear regulations to ensure parasistem functions within legal frameworks while maintaining the integrity of sovereign systems.

- Technical vulnerabilities: Like any technology-driven system, parasistem is prone to cyber threats. Without robust security measures, it could be susceptible to hacking, fraud, or system failures.

- Economic risks: Poorly implemented parasistem frameworks could destabilize economies. Ensuring proper integration with sovereign money systems is crucial to avoid disruptions.

- Integration challenges: Blending centralized and decentralized elements is no easy feat. It requires advanced technology, careful planning, and collaboration between multiple stakeholders to achieve a seamless operation.

Looking Ahead: What’s Next for Parasistem?

- Emerging technologies: Innovations like artificial intelligence, quantum computing, and blockchain are set to revolutionize parasistem. These technologies will enhance efficiency, security, and scalability, making parasistem even more impactful.

- Policy development: Governments need to establish clear guidelines that support parasistem while safeguarding the stability of sovereign money systems. Collaborative efforts between policymakers and tech developers will be key.

- Global cooperation: As financial systems become increasingly interconnected, international collaboration will be essential. Standardized practices and regulations will ensure that parasistem functions smoothly on a global scale.

- Expanding use cases: The versatility of parasistem means it can be applied to various sectors beyond traditional finance. From healthcare to supply chain management, its potential is vast.

Conclusion

Parasistem is more than just a buzzword—it’s a transformative force in the world of finance. By enhancing sovereign money systems, it brings efficiency, inclusivity, and transparency to the forefront. Of course, there are challenges to overcome, from regulatory complexities to technical risks. But with the right approach, parasistem can pave the way for a more stable and innovative financial future.

Key Takeaway: Parasistem enhances sovereign money systems by improving efficiency, boosting security, fostering trust, promoting inclusivity, and ensuring scalability, making financial systems more robust and accessible for everyone.

FAQs

How does parasistem improve financial accessibility?

It creates opportunities for underbanked and underserved communities, making financial systems more inclusive and accessible.

What role does technology play in parasistem?

Parasistem heavily relies on advanced tools like blockchain and AI to enhance transparency, security, and efficiency.

Is parasistem independent of sovereign money systems?

Not entirely. Parasistem is designed to complement sovereign systems, adding layers of efficiency and innovation.

What challenges do governments face with parasistem?

Governments need to navigate regulatory hurdles and create clear policies to balance decentralized features with centralized oversight.

Why is transparency important in parasistem?

Transparency builds trust by showing people how money flows and decisions are made, fostering confidence in the financial system.