Bruce Creighton

Who Really Owns Central Banks? Let’s Clear Up the Confusion

Central banks are often viewed as mysterious, all-powerful entities that pull the strings of the global economy behind closed doors. This perception has led to countless myths and conspiracy theories, particularly regarding who actually owns and controls them. The truth, however, is far more nuanced and grounded in structural design aimed at balancing public accountability with economic stability.

Understanding the ownership of central banks is crucial because these institutions serve as the backbone of a country’s economy. They manage the money supply, set interest rates, and act as the lender of last resort during financial crises. But who holds the keys to these powerful organizations? Let’s demystify the ownership structures of central banks and explore why it matters.

What Do Central Banks Actually Do?

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Before diving into ownership, it is essential to understand the core functions of a central bank. While regular commercial banks provide services like savings accounts and loans to individuals and businesses, central banks operate on a macroeconomic level.

- Printing Money: They are responsible for creating and circulating the national currency, ensuring there is enough liquidity in the system.

- Controlling Inflation and Interest Rates: By adjusting interest rates and managing the money supply, central banks aim to keep inflation in check and prevent the economy from overheating or stalling.

- Regulating Financial Institutions: Central banks oversee commercial banks to ensure they maintain adequate reserves and follow regulations, protecting the broader financial system.

- Lender of Last Resort: During times of severe financial stress, central banks step in to provide emergency funding to failing institutions to prevent systemic collapse.

Famous examples of central banks include the Federal Reserve in the United States, the European Central Bank (ECB), and the Bank of England.

The Three Models of Central Bank Ownership

Ownership models for central banks vary significantly around the world. There is no single “correct” way to structure a central bank, and different countries have adopted models that best suit their historical and political contexts. Generally, these structures fall into three categories:

| Model | Description | Examples |

| Government-Owned | Fully owned by the national government. Profits are typically returned to the state treasury. | Bank of England, Reserve Bank of India (RBI), Bank of Canada, European Central Bank |

| Privately-Owned | Involves private shareholders, often commercial banks. However, these shareholders do not control monetary policy. | Federal Reserve System (USA) |

| Hybrid | A mix of public and private ownership, designed to balance national interests with independent oversight. | Swiss National Bank, Bank of Japan |

1. Government-Owned Central Banks

The most common model globally is full government ownership. In this structure, the central bank is a public institution, and its capital is entirely held by the state. The Bank of England, for example, was nationalized in 1946. Similarly, the Bank of Canada operates as a Crown corporation, meaning it is wholly owned by the federal government but operates with considerable independence from the political process. Any profits generated by these banks—often through interest on loans or government bonds—are handed back to the respective governments. This model emphasizes direct accountability to the public through elected officials.

2. Privately-Owned Central Banks

The concept of a “privately-owned” central bank often sparks the most confusion. The Federal Reserve System in the U.S. is the classic example. It consists of 12 regional Federal Reserve Banks, which are technically owned by the private commercial banks in their respective districts. These member banks are required to hold stock in their regional Fed.

However, this “ownership” does not equate to control. The private shareholders do not dictate monetary policy, nor can they sell or trade their shares. The true decision-making power lies with the Board of Governors in Washington, D.C., whose members are appointed by the President and confirmed by the Senate. The private ownership aspect is largely a structural legacy designed to ensure regional representation and keep the central bank somewhat insulated from day-to-day political pressures.

3. Hybrid Ownership Models

Some central banks blend public and private ownership. The Swiss National Bank (SNB) is a prime example. It is a joint-stock company where the majority of shares are held by public entities (Swiss cantons and cantonal banks), while the remaining shares are traded on the stock market and held by private individuals. Despite having private shareholders who receive a capped dividend, the SNB is governed by a strict mandate to serve the national interest, blending accountability with operational independence.

Debunking Common Myths About Central Banks

The complex structures of central banks, particularly those with private elements, have given rise to persistent myths.

- Myth: Central banks are controlled by secretive private elites. Even in systems with private shareholders, like the Federal Reserve, key monetary policy decisions are made by independent boards or government-appointed officials, not by private bankers seeking personal profit.

- Myth: Central banks operate without oversight. While central banks need operational independence to be effective, they are heavily audited and must regularly report to their governments or legislative bodies.

How Do Ownership Models Handle Political Influence?

A major concern with central banks is how they manage political pressure, especially since their decisions can make or break an economy. The ownership model plays a significant role in this dynamic:

- Government-Owned: Because these banks are fully owned by the state, there is a higher risk of political interference. Politicians might pressure the bank to lower interest rates before an election to create a short-term economic boom, even if it risks long-term inflation. To counter this, countries like Canada and the UK have established strict legal frameworks that grant their central banks operational independence, separating day-to-day monetary policy from political whims.

- Privately-Owned: The inclusion of private shareholders acts as a structural buffer against direct government control. In the U.S. Federal Reserve, for example, the regional banks are owned by private member banks, which helps decentralize power away from Washington. However, the overarching Board of Governors is still politically appointed, ensuring the bank remains accountable to the public rather than private interests.

- Hybrid: These models attempt to strike a balance by distributing ownership among public entities and private investors. The Swiss National Bank’s structure ensures that no single political party or private group can monopolize decision-making, fostering a highly independent environment focused on long-term stability.

How Central Bank Policies Impact the Average Person

While central banks operate at the highest levels of the financial system, their decisions ripple down to affect the daily lives of everyday people. The most direct impact is felt through interest rates. When a central bank raises its benchmark interest rate to combat inflation, commercial banks follow suit. This means higher costs for mortgages, auto loans, and credit card debt, leaving consumers with less disposable income. Conversely, when the central bank lowers rates to stimulate a sluggish economy, borrowing becomes cheaper, encouraging people to buy homes and businesses to expand and hire more workers.

Beyond borrowing costs, central bank policies directly influence inflation and purchasing power. If a central bank increases the money supply too rapidly, the value of the currency can drop, causing the prices of everyday goods—like groceries and gas—to skyrocket. On the other hand, effective monetary policy keeps inflation stable and predictable, protecting the value of your savings and ensuring that your paycheck stretches just as far tomorrow as it does today. Ultimately, the central bank acts as the thermostat for the economy, and its settings determine whether your financial environment feels comfortable or strained.

Why Does Ownership Even Matter?

The ownership structure of a central bank is not just a technical detail; it has real-world implications for how an economy functions.

- Economic Stability: Central banks influence inflation, employment rates, and overall economic growth. The governance structure—dictated by ownership—affects how effectively they can perform these critical tasks without undue interference.

- Accountability vs. Independence: Government-owned banks are directly accountable to the public, but they risk being pressured by politicians seeking short-term economic boosts. Private or hybrid models often provide a buffer, allowing the central bank to make unpopular but necessary long-term decisions.

- Public Trust: Clarity regarding ownership helps build public trust. When citizens understand that their central bank operates with oversight and a mandate for the public good, they are more likely to have confidence in the financial system.

How Do Central Banks Make Money?

A common question is how central banks fund their operations if they don’t rely on taxpayer money. Central banks generate their own income through several channels:

- Interest on Loans: Commercial banks pay interest when they borrow funds from the central bank.

- Government Bonds: Central banks hold large portfolios of government bonds and earn interest on these investments.

- Foreign Exchange: They manage foreign currency reserves and can profit from currency trading and investments.

Crucially, central banks are not profit-driven entities. Any profits left over after covering their operational expenses are typically remitted to the national government (in government-owned models) or distributed as strictly capped dividends to shareholders (in hybrid models).

The Critical Importance of Independence

Whether a central bank is government-owned, privately owned, or a mix of both, the most critical factor for its success is operational independence. Politicians operate on election cycles and often prioritize short-term economic boosts to win votes. Central banks, however, must focus on the long-term health of the economy. If politicians can dictate monetary policy, they might push for lower interest rates or demand the central bank print more money to fund government spending. While this might create a temporary boom, it almost inevitably leads to severe, long-term economic damage—most notably in the form of runaway inflation.

History provides stark, real-world examples of what happens when central bank independence is compromised:

- Turkey (2021–2024): Turkey’s President Recep Tayyip Erdoğan exerted heavy political pressure on the Turkish central bank, firing multiple bank governors who disagreed with his unconventional economic views. Despite rising inflation, Erdoğan demanded the central bank cut interest rates, arguing—contrary to mainstream economics—that high rates cause inflation rather than cure it. The result was disastrous: the Turkish lira lost over 80% of its value against the U.S. dollar, and official inflation soared past 80% in 2022, devastating the purchasing power of ordinary Turkish citizens. It was only after the political pressure eased and the central bank was permitted to aggressively raise rates in 2023 and 2024 that the crisis began to stabilize.

- Argentina (1980s–Present): Argentina has a long and painful history of political interference in its central bank. For decades, successive governments used the central bank as a printing press to finance massive public spending deficits. Because the central bank lacked the independence to push back against political demands, the country suffered through multiple devastating bouts of hyperinflation—including a catastrophic peak of over 3,000% in 1989. Even today, the legacy of this political interference continues to haunt the Argentine economy with chronic instability and persistently high inflation rates, serving as a cautionary tale for the rest of the world.

These examples underscore a fundamental truth: when a central bank loses its independence, it is the ordinary citizen—not the politician—who pays the price through eroded savings, higher prices, and economic hardship.

The Bottom Line

Central banks might seem like mysterious entities, but their ownership structures are deliberately designed to ensure balance, transparency, and stability. By understanding how they work, who truly controls them, and why their independence is so fiercely protected, we can demystify the financial system and recognize their vital role in keeping the global economy on track.

FAQs

1. What sets a central bank apart from a regular bank?

A central bank oversees and manages a country’s entire monetary system and currency. Regular commercial banks, on the other hand, provide direct financial services like savings accounts, mortgages, and credit cards to individuals and businesses.

2. Are central banks completely independent from the government?

Not entirely. While many central banks operate with operational independence to avoid short-term political interference, they are still bound by mandates set by the government and have accountability mechanisms, such as regular reporting to legislative bodies, to ensure transparency.

3. Can a central bank ever run out of money?

Not in the traditional sense. Central banks have the unique authority to create money (often digitally). However, doing so recklessly or excessively can lead to severe inflation, devaluing the currency.

4. Do central banks make money simply by printing currency?

No. Printing money is a tool for controlling economic liquidity, not a source of profit. Central banks earn their income primarily through interest on loans to commercial banks and returns on investments like government bonds.

5. Why is the Federal Reserve’s structure considered unique?

The Federal Reserve utilizes a hybrid structure. It has private member banks that hold non-transferable shares in regional Reserve Banks, but the overarching control and monetary policy decisions are handled by the Board of Governors, who are appointed by the U.S. government. This model aims to balance regional banking representation with national public oversight.

From Stress to Success: 11 Actionable Budgeting Tips for Real Financial Freedom

Frequently Asked Questions (FAQ)

1. How long does it take to get used to a budget?

It typically takes about 90 days to turn budgeting into a consistent habit. The first month is about tracking and awareness, the second is about refining your categories, and by the third month, the process should feel much more natural. Be patient with yourself.

2. What if my income is irregular? How do I budget?

Budgeting with an irregular income is challenging but crucial. The key is to budget based on your lowest-earning month from the past year. This creates a baseline. In months where you earn more, use the extra income to aggressively build your emergency fund, pay down debt, or save for large, specific goals. This smooths out the financial peaks and valleys.

3. Are budgeting apps better than a spreadsheet?

It depends on your personality. Budgeting apps like YNAB or Monarch Money are excellent for automating tracking and providing real-time insights, which can be very motivating. A spreadsheet offers more control and customization and is completely free. The best tool is the one you will use consistently.

4. I’ve tried budgeting before and failed. What makes this time different?

Most budgets fail because they are too restrictive or they lack a clear “why.” This time, focus on progress, not perfection. Start with the 50/30/20 rule as a guideline, not a rigid law. Most importantly, connect your budget to exciting, motivating goals. When you know your savings are building toward a dream vacation or a debt-free life, it’s much easier to say no to small, impulsive purchases.

5. Can I still have fun while on a budget?

Absolutely. In fact, a good budget *gives you permission* to spend money on fun, guilt-free. The “Wants” category (typically 30% of your income) is specifically for dining out, hobbies, and entertainment. By planning for these expenses, you can enjoy them without worrying that you are neglecting your financial responsibilities.

How Inflation Affects Your Savings and Purchasing Power in 2026

A Closer Look at Recent Inflation: 2025–2026

To provide a clearer picture of the current economic environment, let’s examine the recent inflation trends in both the United States and Canada, and see how they compare to the turbulent years that preceded them.

United States Inflation at a Glance

In the U.S., the annual inflation rate for 2025 was 2.7%, a meaningful moderation from the 2.9% rate seen in 2024 and a dramatic improvement from the 8.0% peak recorded in 2022. This cooling trend has continued into early 2026, with the annual rate holding steady at 2.4% through February 2026. [1]

| Year | US Annual Inflation Rate | Key Driver |

|---|---|---|

| 2021 | 7.0% | Post-pandemic supply chain disruptions, stimulus spending |

| 2022 | 8.0% | Energy price spike (Russia-Ukraine war), persistent supply shortages |

| 2023 | 4.1% | Shelter costs, sticky services inflation |

| 2024 | 2.9% | Shelter costs moderating; food and energy stabilizing |

| 2025 | 2.7% | Food away from home (+4.1%), medical care (+3.2%), gasoline declining (-3.4%) |

| 2026 YTD (Jan) | 2.4% | Continued moderation in shelter and energy costs |

Sources: U.S. Bureau of Labor Statistics [1], Minneapolis Federal Reserve [2]

The key drivers behind U.S. inflation in 2025 were food away from home (up 4.1%), medical care (up 3.2%), and shelter costs. On the positive side, gasoline prices fell 3.4% for the third consecutive year, providing meaningful relief at the pump. The Federal Reserve’s sustained interest rate policy has been central to bringing inflation down from its 2022 peak. To understand more about how the Fed manages this process, see our article on how the Federal Reserve controls inflation.

Canada Inflation at a Glance

Canada has seen a more pronounced cooling of inflation, with the annual average rate for 2025 at 2.1%, down from 2.4% in 2024 and well below the 6.8% peak of 2022. The rate for January 2026 was 2.3%. [3]

| Year | Canada Annual Inflation Rate | Key Driver |

|---|---|---|

| 2021 | 3.4% | Post-pandemic demand surge, supply chain issues |

| 2022 | 6.8% | Energy prices, food costs, shelter |

| 2023 | 3.9% | Mortgage interest costs, rent, food |

| 2024 | 2.4% | Shelter (mortgage interest +20.1%, rent +8.2%), food |

| 2025 | 2.1% | Grocery prices (+3.5%), rent (+5.0%), energy declining (-5.7%) |

| 2026 YTD (Jan) | 2.3% | Slight uptick driven by food and shelter |

Sources: Statistics Canada [3] [4]

A notable factor in Canada’s 2025 inflation story was the removal of the consumer carbon price in April 2025, which significantly reduced gasoline and natural gas prices. However, grocery prices accelerated sharply, rising 3.5% on average — driven by a 13.5% jump in fresh beef prices, higher coffee costs due to adverse weather in growing regions, and the impact of retaliatory tariffs on U.S. goods. Rent prices, while slowing from the 8.2% surge of 2024, still rose 5.0% nationally and have climbed a staggering 28.5% since 2020. [3]

Frequently Asked Questions

1. What is the difference between inflation and the cost of living?

Inflation is the rate at which the general level of prices for goods and services is rising, while the cost of living is the total amount of money needed to sustain a certain standard of living in a particular place. Inflation is a major driver of rising living costs, but the cost of living also reflects local factors like taxes, housing markets, and wage levels. Two cities can have the same inflation rate but very different costs of living.

2. How does the government measure inflation?

The most common measure is the Consumer Price Index (CPI), which tracks the average change in prices paid by consumers for a fixed “basket” of goods and services — things like groceries, rent, gasoline, and healthcare. In the U.S., the Bureau of Labor Statistics (BLS) publishes the CPI monthly. In Canada, Statistics Canada does the same. The CPI is the number you hear quoted most often when news reports discuss the inflation rate.

3. Can inflation ever be a good thing?

A small, steady amount of inflation — typically around 2% annually — is generally considered a sign of a healthy, growing economy. It encourages spending and investment, because consumers and businesses are motivated to act now rather than wait for prices to rise further. It also gives central banks room to cut interest rates during downturns. The problem arises when inflation runs too hot for too long, eroding purchasing power faster than wages can keep up.

4. What is “core inflation” and why does it matter?

Core inflation excludes the volatile categories of food and energy from the CPI calculation. Because food and energy prices can swing dramatically due to temporary factors — a drought, a geopolitical conflict, a cold winter — economists and central banks often focus on core inflation to get a clearer picture of the underlying, persistent inflation trend. When the Federal Reserve or the Bank of Canada sets interest rate policy, core inflation is one of the most important numbers they watch.

5. How can I track the current inflation rate?

You can find the latest official inflation data directly from the government agencies that calculate it. For the United States, visit the U.S. Bureau of Labor Statistics CPI page. For Canada, visit the Statistics Canada Consumer Price Index portal.

**References**

[1] Bureau of Labor Statistics, U.S. Department of Labor, _The Economics Daily_, “Consumer Price Index: 2025 in review,” January 21, 2026. https://www.bls.gov/opub/ted/2026/consumer-price-index-2025-in-review.htm

[2] Federal Reserve Bank of Minneapolis, “Consumer Price Index, 1913–.” https://www.minneapolisfed.org/about-us/monetary-policy/inflation-calculator/consumer-price-index-1913-

[3] Statistics Canada, _The Daily_, “Consumer Price Index: Annual review, 2025,” January 19, 2026. https://www150.statcan.gc.ca/n1/daily-quotidien/260119/dq260119b-eng.htm

[4] Statistics Canada, _The Daily_, “Consumer Price Index, January 2026,” February 17, 2026. https://www150.statcan.gc.ca/n1/daily-quotidien/260217/dq260217a-eng.htm

How to Get Your Free Annual Credit Report

Quick Summary: Getting Your Free Annual Credit Report

- Who is eligible: Every U.S. consumer is entitled to one free credit report per year from each of the three major bureaus.

- Where to get it: The only federally authorized source is AnnualCreditReport.com.

- What it costs: Completely free — no credit card required.

- How often: Once per year from each bureau (Equifax, Experian, TransUnion); currently available weekly due to a pandemic-era extension.

- Why it matters: Errors on your credit report can lower your score and affect loan approvals, interest rates, and even employment.

Your credit report is one of the most important financial documents you will ever review — yet most people have never looked at theirs. In the United States, federal law gives every consumer the right to access a free copy of their credit report from each of the three major credit bureaus once every twelve months. Knowing how to access, read, and act on this report is a foundational financial skill, particularly if you are planning to apply for a debt consolidation loan, mortgage, or any other form of credit.

To secure your free annual credit report, visit the authorized website and follow the simple steps provided. It is essential to utilize this opportunity to keep track of your financial health.

What Is a Credit Report and Why Does It Matter?

A credit report is a detailed record of your borrowing history. It includes information about every credit account you have opened, your payment history on those accounts, the balances you currently carry, any public records such as bankruptcies or judgments, and a list of recent inquiries made by lenders when you applied for credit.

Lenders use your credit report — along with the credit score derived from it — to assess how likely you are to repay a loan. A report with errors, outdated negative information, or signs of identity theft can artificially lower your score and cost you thousands of dollars in higher interest rates over the life of a loan. Reviewing your report regularly is the only way to catch and correct these problems before they affect a major financial decision.

Where to Get Your Free Annual Credit Report

Obtaining your free annual credit report is straightforward. The process is designed to ensure that you can manage your credit effectively and understand your financial standing.

The only website authorized by the U.S. federal government to provide free annual credit reports is AnnualCreditReport.com. This site was created jointly by Equifax, Experian, and TransUnion in compliance with the Fair Credit Reporting Act (FCRA). There is no charge, and you do not need to provide a credit card number.

Be cautious of impostor sites. Websites with similar-sounding names are not the official source and may charge fees or enroll you in subscription services. Always go directly to AnnualCreditReport.com or call 1-877-322-8228.

Remember to check your free annual credit report regularly for any inaccuracies that could impact your credit score.

How Often Can You Access Your Report for Free?

Under the FCRA, you are entitled to one free report per bureau per year — meaning three reports in total annually. Since the COVID-19 pandemic, the three bureaus have extended free weekly access through AnnualCreditReport.com. A practical strategy is to stagger your requests — pulling one bureau’s report every four months — so you have a rolling view of your credit throughout the year.

By accessing your free annual credit report, you can stay informed about your credit status and take necessary actions if needed.

Step-by-Step: How to Request Your Free Credit Report

-

- Visit AnnualCreditReport.com directly in your browser.

You can easily access your free annual credit report online by visiting the official site.

-

- Select the bureaus you want to request from. You can request all three at once or stagger them.

- Verify your identity by providing your name, address, Social Security number, and date of birth.

- Review your report online or download a PDF copy for your records.

- Dispute any errors directly with the bureau that reported the incorrect information.

If errors are found in your free annual credit report, it’s crucial to dispute them promptly to maintain an accurate credit profile.

What to Look for When Reviewing Your Report

Checking your free annual credit report helps you verify that all personal information is correct and up to date.Make sure to analyze the account history section of your free annual credit report for any discrepancies.Your free annual credit report should reflect accurate balances to avoid any confusion regarding your financial obligations.Inquiries listed in your free annual credit report can affect your credit score, so ensure they are legitimate.

| Section | What to Check | Red Flags |

|---|---|---|

| Personal Information | Name, address, employer | Unfamiliar addresses or names (possible identity theft) |

| Account History | Open/closed accounts, balances, payment history | Accounts you do not recognize; disputed late payments |

| Public Records | Bankruptcies, judgments, liens | Records that are outdated or inaccurate |

| Inquiries | Hard and soft credit pulls | Hard inquiries from lenders you never applied to |

How to Dispute Errors on Your Credit Report

If you find an error, you have the right to dispute it. Each bureau has an online dispute portal. Bureaus are required by law to investigate disputes within 30 days. If the information cannot be verified, it must be removed. If you believe a lender or bureau has violated your rights under the FCRA, you can submit a complaint to the Consumer Financial Protection Bureau (CFPB).

When disputing errors in your free annual credit report, be sure to follow the correct procedures established by the bureaus.

How Your Credit Report Connects to Debt Consolidation

If you are considering a debt consolidation loan, reviewing your credit report first is an essential step. Reviewing your report before you apply gives you the opportunity to dispute errors, understand your current standing, and identify which debts are dragging your score down. For a full walkthrough of how consolidation affects your credit over time, see our guide on how debt consolidation can improve your credit score. For a beginner’s overview of the consolidation process itself, start with How Debt Consolidation Loans Work: A Beginner’s Guide.

Understanding your free annual credit report is critical before applying for any loans to ensure you are making informed decisions.

How to Get Your Free Credit Report: Canada vs. the United States

The process for obtaining a free credit report differs significantly between Canada and the United States. Understanding these differences ensures you are using the correct, official channels and not inadvertently paying for something that is available to you at no cost.

The differences in accessing a free annual credit report between countries highlight the importance of knowing your rights.

Free Credit Reports in Canada

Canada has two national credit bureaus: Equifax Canada and TransUnion Canada. Unlike the United States, there is no single government-authorized website for accessing your reports. Instead, you request directly from each bureau, and there is no annual limit — you may request your report as often as you wish.

Both bureaus offer free online access to your full credit report, updated monthly. You may also request by mail (with two pieces of ID), by phone, or in person at a bureau office. One important nuance: while the credit report is free, your credit score may not always be included at no cost unless you live in Quebec or use a third-party service such as Credit Karma. Requesting your own report does not affect your credit score.

Free Credit Reports in the United States

Your free annual credit report can help you monitor your financial health and prevent identity theft.

In the United States, federal law guarantees every consumer access to one free credit report per year from each of the three major bureaus: Equifax, Experian, and TransUnion. The only government-authorized source is AnnualCreditReport.com. Many look-alike websites exist that charge fees — always use the official site.

Reports can be requested online, by phone, or by mail. During certain periods (such as the post-pandemic era), the bureaus have offered free weekly access. Credit scores are not included in the free report by default.

Utilizing your free annual credit report is a proactive way to manage your financial affairs.

Key Differences at a Glance

| Feature | Canada | United States |

|---|---|---|

| Number of bureaus | 2 (Equifax, TransUnion) | 3 (Equifax, Experian, TransUnion) |

| Free report frequency | Unlimited (varies by method) | Once per year per bureau |

| Free online access | Yes (directly via each bureau) | Yes (via AnnualCreditReport.com only) |

| Free credit score included | Sometimes (Equifax monthly; Credit Karma) | Not included by default |

| Government-authorized site | None — request directly from bureaus | AnnualCreditReport.com |

For Canadian readers, the key takeaway is to check both bureaus regularly, since lenders may report to one and not the other. For U.S. readers, always use AnnualCreditReport.com exclusively — it is the only site authorized by federal law, and using it will never result in a charge.

Always remember to access your free annual credit report to stay informed about your credit status.

Frequently Asked Questions

What is the difference between a credit report and a credit score?

A credit report is a detailed history of your borrowing and repayment activities. A credit score is a single three-digit number (like a FICO or VantageScore) that summarizes the risk of lending to you, based on the information in your report. Your free annual report shows your history, but the score is usually a separate, paid product.

How long does it take to fix an error on my credit report?

Under the FCRA, the credit bureaus generally have 30 to 45 days to investigate and resolve a dispute after you file it. The process involves them contacting the creditor that supplied the information to verify its accuracy. If the creditor confirms the error or does not respond, the bureau must remove the item.

Should I pay for a credit monitoring service?

For most people, it is not necessary. Between free annual reports, free scores from your credit card provider, and the ability to place free fraud alerts or credit freezes, you can monitor your own credit effectively at no cost. Paid services are often expensive and offer services you can perform yourself for free.

What should I do if I am denied credit based on my report?

If you are denied credit, a loan, or even insurance, the lender must provide you with an “adverse action notice.” This notice tells you which credit bureau’s report was used and informs you of your right to request a free copy of that specific report within 60 days.

What is the difference between a fraud alert and a credit freeze?

A fraud alert is a notice on your report that requires lenders to take extra steps to verify your identity before opening new credit. It lasts for one year. A credit freeze is more restrictive — it locks your report entirely, preventing any new creditors from accessing it until you lift it. Both are free services available from all three bureaus.

What information is NOT included in my credit report?

Your credit report does not contain information about your race, religion, national origin, marital status, political affiliation, medical history, or criminal record. It is focused solely on your financial history with credit and debt.

Does requesting my own credit report hurt my score?

No. Requesting your own credit report is a “soft inquiry” and has no effect on your credit score.

Is AnnualCreditReport.com safe?

Yes. It is the only federally mandated free credit report service, regulated under the FCRA.

Can Canadians access their credit reports for free?

Yes. In Canada, Equifax and TransUnion both offer free annual credit reports. Equifax also offers free online access.

Every debt situation is unique. If you’d like a one-on-one consultation with Bruce Creighton, CPA — with 35 years of financial experience — to review your credit report and debt consolidation options, contact us here.

How to Use Debt Consolidation to Improve Your Credit Score (5 Ways That Work)

")

Introduction

Debt consolidation to improve your credit score works by lowering your credit utilization, simplifying your payments, and reducing the risk of missed due dates. When used strategically, consolidation becomes a tool that strengthens your financial profile instead of weakening it. This guide explains how consolidation affects your credit report, what improves your score, what can temporarily lower it, and how to choose the right consolidation method.

What Is Debt Consolidation?

Debt consolidation means combining multiple high‑interest debts into one new loan or line of credit—usually with a lower interest rate and a single monthly payment. Common consolidation tools include:

- Personal loans

- Balance‑transfer credit cards

- Home equity loans or HELOCs

- Debt management programs

Consolidation doesn’t erase your debt, but it restructures it in a way that can improve your credit score over time.

To learn more about key terms, visit our Debt Consolidation Glossary.

How Debt Consolidation Improves Your Credit Score

1. It Lowers Your Credit Utilization Ratio

Credit utilization is one of the biggest factors in your credit score. When you consolidate credit card balances into a personal loan, your revolving utilization drops—often dramatically.

Lower utilization = higher credit score.

2. It Helps You Avoid Missed Payments

Payment history makes up 35% of your credit score. Consolidation replaces multiple due dates with one predictable payment, reducing the chance of late or missed payments.

You can estimate your savings using our Debt Consolidation Calculator.

3. It Can Reduce Your Interest Costs

Lower interest means more of your payment goes toward principal. As balances fall faster, your credit score improves.

4. It Creates a More Predictable Repayment Schedule

A fixed‑rate consolidation loan gives you a clear payoff timeline. This stability helps lenders view you as lower risk.

5. It Can Improve Your Credit Mix

Credit mix accounts for 10% of your score. Adding an installment loan (personal loan) to your existing revolving credit (credit cards) can improve your score slightly.

When Debt Consolidation Can Hurt Your Credit Score

Debt consolidation can temporarily lower your score if:

- You apply for multiple loans in a short period (hard inquiries)

- You close old credit card accounts (reduces credit history length)

- You continue using your credit cards after consolidating

- Your new loan increases your total debt load

These effects are usually short‑term and reverse as you make consistent payments. For more information about how credit scores work, visit the Consumer Financial Protection Bureau.

How Long It Takes to See Credit Score Improvements

Most people see improvements within 30–90 days, depending on:

- How much utilization drops

- Whether payments are made on time

- Whether old credit card balances stay at zero

- Whether new debt is avoided

How to Choose the Right Debt Consolidation Option

Personal Loan

Best for: predictable payments, lowering utilization, reducing interest.

Balance‑Transfer Credit Card

Best for: paying off debt within 12–18 months with 0% APR.

Debt Management Program

Best for: lowering interest rates without taking out a new loan.

Home Equity Loan / HELOC

Best for: homeowners with strong credit and stable income.

Frequently Asked Questions

Does debt consolidation improve your credit score?

Debt consolidation can improve your credit score by lowering your credit utilization, reducing missed payments, and simplifying your repayment schedule.

How long does it take to see credit score improvements?

Most people see improvements within 30–90 days as utilization drops and on‑time payments begin to build positive history.

Can debt consolidation hurt your credit score?

It can temporarily lower your score due to a hard inquiry and a new account, but these effects fade quickly when you make consistent payments.

The Gold Standard Debate: Should We Return to Backed Money?

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Explore the gold standard debate — should modern economies return to gold-backed money, or is fiat currency the better path forward?

Introduction: Why The Gold Standard Debate Still Matters Today

If there’s one topic that never seems to lose its shine in economic circles, it’s the gold standard debate. From YouTube finance influencers to policymakers and everyday savers, many are asking: Should we bring back money backed by gold?

The question isn’t just about nostalgia for shiny coins or distrust in “paper money.” It cuts to the heart of how value is created, stored, and protected in our financial system. In an age of inflation fears, digital currencies, and mounting government debt, people are searching for a system that feels real again — one grounded in something tangible.

So, should we go back to the gold standard? Or has the world moved beyond it for good?

Let’s unpack the history, arguments, and real-world implications — and see how this debate connects directly to your financial life today.

️ What Was the Gold Standard?

The gold standard was a monetary system where a country’s currency was directly tied to a specific amount of gold. For example, under the U.S. gold standard of the early 20th century, $35 equaled one ounce of gold. That meant every dollar in circulation could theoretically be exchanged for gold held in government vaults.

This system limited how much money could be created. The government couldn’t print more money unless it had more gold to back it up. Supporters say that kept inflation low and disciplined public spending.

Types of Gold Standards:

- Classical Gold Standard (1870–1914): Money was fully convertible to gold, and global trade was stable.

- Gold Exchange Standard (1925–1931): Countries held foreign currencies (like U.S. dollars or British pounds) backed by gold.

- Bretton Woods System (1944–1971): The U.S. dollar was pegged to gold, and other nations pegged their currencies to the dollar.

When President Richard Nixon ended dollar convertibility to gold in 1971, the world entered the era of fiat money — currency not backed by a commodity, but by government decree and economic trust.

⚖️ Fiat Money vs. Gold-Backed Money: What’s the Real Difference?

The debate often boils down to control versus stability.

Feature Gold-Backed Money Fiat Money

Value Basis Linked to a physical commodity (gold) Based on government trust and regulation

Money Supply Control Limited by gold reserves Determined by central banks

Inflation Control Naturally constrained Requires policy discipline

Economic Flexibility Restricted (limited stimulus) Highly flexible

Historical Stability Long-term stable prices Prone to inflation and crises

Crisis Response Slow — limited tools Quick — central banks can print money

Fiat systems allow nations to respond to crises like COVID-19 or financial crashes by injecting liquidity. But critics argue this power often leads to debt bubbles, currency devaluation, and inequality.

“Gold Standard vs. Fiat Money Comparison Template”

Use this simple template to compare how each system affects you personally.

Reflect and fill in your own observations.

Category Gold Standard System Fiat System (Today’s Money) Your Reflection

Money Creation Backed by physical gold reserves Created digitally or through lending _______________

Inflation Impact Historically low Often higher, depends on policy _______________

Savings Power Stable value over time Subject to erosion by inflation _______________

Debt and Borrowing Limited government borrowing High debt flexibility _______________

Economic Growth Slower but steadier Faster but volatile _______________

Financial Stability Hard money discipline Dependent on trust and regulation _______________

Personal Comfort Level Tangible security Policy-driven confidence _______________

Tip: Use this template as part of your personal financial education journal — track how your beliefs about money evolve as you understand the system better.

The Case For the Gold Standard

Advocates believe that returning to gold-backed money could restore trust and discipline in the economy. Here are the key arguments:

1. Inflation Control

Because money creation would be limited by gold reserves, governments couldn’t inflate away debt or overspend.

2. Fiscal Discipline

The gold standard forces governments to live within their means — reducing reckless deficit spending and long-term debt accumulation.

3. Stable Value

Over centuries, gold has retained its value better than any fiat currency. This stability can restore confidence for savers and investors.

4. Global Trust

A universal gold-based system could stabilize international exchange rates and reduce speculative currency wars.

As economist Milton Friedman once said:

“Inflation is taxation without legislation.”

The gold standard, in theory, prevents that kind of hidden tax.

The Case Against the Gold Standard

Critics argue that while gold may shine, it can also trap economies in rigidity.

1. Limited Flexibility

In times of crisis, such as the Great Depression, the gold standard prevented central banks from increasing the money supply to revive the economy.

2. Deflation Risk

When money supply can’t expand, prices fall — leading to wage cuts, job losses, and economic stagnation.

3. Resource Dependence

Economic growth would depend on mining more gold — not innovation or productivity.

4. Unequal Gold Distribution

Countries rich in gold (like the U.S. post–World War II) would dominate, leaving others vulnerable to external shocks.

5. Not Fit for the Digital Age

Modern economies rely on electronic transfers, derivatives, and dynamic credit systems — not physical metal locked in vaults.

A Balanced View: Could a Partial Gold Standard Work?

Some economists propose a hybrid system — where currencies are partially backed by gold, digital assets, or a commodity basket.

This could combine the stability of hard assets with the flexibility of fiat systems.

For example:

- The International Monetary Fund (IMF) has explored “Special Drawing Rights” (SDRs) as a diversified reserve currency.

- Central banks could issue digital currencies (CBDCs) with fractional gold backing to maintain public confidence.

Such innovations could represent a “Gold Standard 2.0” — not a step backward, but an evolution toward responsible money creation.

Trending Question: Would Returning to the Gold Standard Stop Inflation?

This is one of the most common questions driving the gold standard debate with strong arguments on both sides.

In theory, yes — tying money to gold would limit inflation by limiting the money supply and imposing fiscal discipline. But in practice, it is not guaranteed to stop inflation and could limit economic growth and increase unemployment during downturns resulting in economic instability and a loss of monetary policy flexibility to manage it.

The U.S. Congressional Research Service (CRS) notes that the Great Depression worsened because the gold standard restricted government action (source: crsreports.congress.gov).

Meanwhile, the Federal Reserve explains that fiat flexibility has helped stabilize output and prices since 1971 (federalreserve.gov).

So, while gold backing could discipline policy, it’s not a magic cure. The real solution lies in responsible governance, not just shiny metal.

What It Means for You: How This Debate Impacts Your Finances

Even if we never return to a gold standard, understanding this debate helps you make smarter decisions.

✅ 1. Inflation Awareness

Knowing how fiat systems work helps you protect your savings with inflation-hedged assets (like TIPS, real estate, or diversified ETFs).

✅ 2. Diversified Investing

Gold can be part of a balanced portfolio — not because of nostalgia, but as a hedge against monetary uncertainty.

✅ 3. Debt Perspective

In fiat systems, debt is a feature, not a flaw. Understanding this lets you navigate credit systems and government borrowing logically.

✅ 4. Critical Thinking

When politicians or influencers promise “sound money” through gold, you’ll be able to ask: How would that affect jobs, liquidity, and growth?

To deepen your understanding:

Internal Links (TheMoneyQuestion.org)

- Who Really Controls the Money? A Look at Central Banks

- The Debt Myth: Why Government Borrowing Isn’t Like a Household Budget

External Links

-

Federal Reserve History – The End of the Gold Standard https://www.federalreservehistory.org/essays/gold-standard

Overview from the Federal Reserve on why the U.S. ended gold convertibility in 1971 and the long-term economic implications. -

Congressional Research Service (CRS) – Returning to the Gold Standard: Historical and Policy Perspectives

https://crsreports.congress.gov/product/pdf/R/R43890

A nonpartisan U.S. government analysis explaining the potential effects of reinstating a gold-backed monetary system. -

Investopedia – What Is the Gold Standard?

→ https://www.investopedia.com/terms/g/goldstandard.asp

Educational reference summarizing the gold standard’s history, advantages, and disadvantages in accessible language.

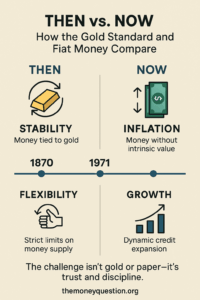

“Then vs. Now: How the Gold Standard and Fiat Money Compare”

Sections:

- Visual timeline (1870 → 1971 → Today)

- Icons for stability, inflation, flexibility, and growth

- Key takeaway: “The challenge isn’t gold or paper — it’s trust and discipline.”

- Add footer: themoneyquestion.org

Key Takeaways

- The gold standard offered stability, but limited flexibility.

- Fiat money offers flexibility, but risks inflation and overspending.

- The best system may blend discipline with innovation.

- Understanding money’s foundation empowers smarter financial choices.

Conclusion: Beyond the Gold Standard Debate

The gold standard debate isn’t just academic — it’s about who controls money, and how that control affects your life.

Whether we back currency with gold, digital code, or trust, the key issue remains accountability.

If citizens understand money creation, demand transparency, and make informed personal choices, the system becomes stronger — whatever form it takes.

Gold isn’t the answer. But the discipline it represents might be the one lesson modern money still needs.

FAQs: The Gold Standard Debate

1. What was the purpose of the gold standard?

The gold standard aimed to ensure monetary stability by tying each unit of currency to a fixed quantity of gold. This limited governments from creating money arbitrarily and helped control inflation. It also made international trade smoother because exchange rates were predictable and trusted.

2. Why did the U.S. abandon the gold standard?

The U.S. left the gold standard in 1971 when President Nixon ended convertibility to preserve economic flexibility. Global trade imbalances and postwar spending made it impossible to maintain fixed gold prices. Moving to fiat money allowed the government and Federal Reserve to respond more effectively to inflation, unemployment, and recession pressures.

3. Would a return to gold stop inflation permanently?

A gold-backed system could reduce inflation by limiting the money supply, but it wouldn’t eliminate it entirely. Prices also depend on productivity, wages, and global demand. Historically, gold standards have sometimes caused deflation, which can be just as harmful as inflation.

4. Is gold-backed money safer than fiat money?

Gold-backed money can feel safer because its value is linked to a tangible asset rather than government trust. However, this safety comes at the cost of flexibility — governments can’t easily stimulate growth or respond to crises. Fiat systems rely on policy discipline instead of metal reserves for stability.

5. Can digital currencies be gold-backed?

Yes, several new technologies allow for digital currencies partially backed by gold. Central Bank Digital Currencies (CBDCs) or stablecoins could use gold reserves to ensure value stability while allowing digital efficiency. This hybrid model combines traditional trust with modern innovation.

6. What caused the Great Depression under the gold standard?

During the Great Depression, the gold standard limited how much money governments could create to boost their economies. As prices and wages fell, deflation deepened the downturn. Countries that left the gold standard earlier — like the U.K. — recovered faster than those that stayed tied to it.

7. Does any country use the gold standard today?

No major economy operates on the gold standard today; all use fiat money issued by central banks. However, countries like Switzerland and Singapore maintain strong gold reserves as part of their financial security strategy. Gold remains an important reserve asset, even without direct convertibility.

8. Should investors buy gold now?

Gold can be a good diversification tool, especially during times of inflation or market uncertainty. Financial advisors often recommend allocating 5–10% of your portfolio to gold or similar assets. It’s not about betting on a gold standard comeback — it’s about hedging against fiat volatility.

9. What are the pros of fiat money?

Fiat money gives governments and central banks the flexibility to manage the economy, fund public programs, and respond to crises. It allows for credit expansion and innovation, which drive growth. The challenge is maintaining discipline so that flexibility doesn’t lead to runaway inflation.

10. What’s the biggest takeaway from the gold standard debate?

The real question isn’t whether we should return to gold — it’s whether we can create a responsible and transparent monetary system. Sound money depends more on good governance and informed citizens than on any metal. Understanding both systems empowers you to make better financial and policy judgments.

Affiliate Disclosure

Some links on this page may be affiliate links. This means we may earn a small commission at no extra cost to you if you purchase through them.

Disclaimer: The content provided is for informational purposes only and is not a substitute for professional financial or legal advice.

A Brief History of Money and Banking

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Discover how money and banking evolved—from ancient trade to banking in the Middle Ages—and what it reveals about today’s financial system.

Introduction: The Long Journey of Money and Banking

Money didn’t start as coins, paper, or digital code. It began as trust. From seashells and salt to gold coins and digital ledgers, the story of money is really a story about how humans organize trust, power, and value.

In this post, we’ll explore banking in the Middle Ages, the roots of modern finance, and what these historical lessons can teach you about money management today.

By the end, you’ll understand:

-

How early banking systems laid the groundwork for today’s economy

-

Why medieval innovations like bills of exchange changed everything

-

How understanding the past can help you make smarter financial decisions today

Before the Banks: Barter and Early Exchange

Long before credit cards and online transfers, humans relied on barter—trading goods and services directly.

But barter was inefficient. A farmer with wheat might not need a fisherman’s catch. This “double coincidence of wants” problem forced societies to find a common medium of exchange—something durable, portable, and universally accepted.

The Birth of Commodity Money

-

Early forms of money included cattle, shells, salt, silver, and gold.

-

By 2500 BCE, the Sumerians recorded transactions on clay tablets, one of the earliest examples of accounting.

-

The Code of Hammurabi (circa 1750 BCE) outlined interest rates and loan contracts, showing how old money management really is.

Money simplified trade, but it also required new systems of record-keeping, lending, and regulation—the precursors of banking.

Temples, Merchants, and the First “Banks”

Before there were bankers, there were priests. In Mesopotamia, temples held grain and precious metals for safekeeping. People deposited their valuables, and the temple lent resources to others—collecting interest as profit.

This early system mirrored modern banking principles:

-

Deposits: People entrusted goods to a trusted intermediary.

-

Loans: Those resources were lent to others.

-

Interest: The intermediary profited by lending at a higher rate.

By the time of ancient Greece and Rome, moneylenders—called trapezitai in Greek—handled deposits, loans, and currency exchange. In Rome, bankers (argentarii) even recorded transactions in ledgers similar to modern account books.

The Collapse of Rome and the Dormant Centuries

When the Roman Empire fell in the 5th century, Europe’s trade networks disintegrated. Roads decayed, cities emptied, and coins became scarce. The idea of “banking” all but disappeared.

But not everywhere.

In the Islamic world, scholars preserved and expanded financial knowledge. Islamic banking principles—rooted in partnerships and profit-sharing rather than interest—thrived from Baghdad to Cordoba.

These ideas would later influence European banking practices during the Middle Ages.

Banking in the Middle Ages: The Birth of Modern Finance

Banking in the Middle Ages—marks a turning point in financial history.

Between the 11th and 15th centuries, European commerce revived, trade routes reopened, and merchants needed safer, faster ways to move money across distances. Carrying gold was dangerous and inefficient, so they turned to paper instruments, early credit systems, and trusted financial intermediaries.

The Italian Banking Renaissance

The story begins in Italy, the heart of medieval trade. Cities like Venice, Florence, and Genoa became bustling hubs of commerce—and innovation.

Key Developments:

-

Bills of Exchange: Merchants could pay with paper instead of coins. These acted like early checks, allowing someone to deposit money in one city and withdraw it in another.

-

Merchant Banks: Families like the Medici of Florence created banking houses that offered currency exchange, loans, and investment services.

-

Double-Entry Bookkeeping: A revolutionary accounting method (first codified by Luca Pacioli in 1494) made it easier to track profits and losses accurately.

This was the dawn of financial literacy. Banking became systematic, and the word “bank” itself derived from banca—the Italian word for “bench,” where moneylenders once did business.

Faith, Trust, and Regulation in Medieval Finance

In the Middle Ages, money was not just economics—it was morality.

The Catholic Church forbade usury (charging interest), believing it sinful to profit from lending. But trade demanded credit, so bankers found creative ways around the rule—charging “fees” or “exchange rates” instead of explicit interest.

Meanwhile, trust became the currency of commerce. Banks held vast power but depended on reputation. A single rumor could trigger a medieval bank run, collapsing fortunes overnight—just as it can today.

Case Study: The Medici Bank

The Medici Bank (1397–1494) is often considered the blueprint of modern banking.

Founded by Giovanni di Bicci de’ Medici, it grew into a financial empire spanning Europe. The Medici family financed kings, popes, and trade expeditions—while pioneering practices like:

-

Branch banking (offices across cities)

-

Letters of credit (predecessors to modern wire transfers)

-

Partnership management structures

However, political entanglements and risky loans eventually led to the bank’s downfall—a timeless reminder that over-leverage and corruption destroy even the strongest institutions.

The Birth of National Banks

As Europe entered the Renaissance, monarchs realized they needed centralized systems to finance wars and trade. This led to additional developments to money and banking as financiers adapted to changing requirements of users of the financial system.

The Bank of Amsterdam (1609) became one of the first public banks, followed by the Bank of England (1694), which introduced the concept of fractional reserve banking—holding only a fraction of deposits in reserve while lending out the rest.

This innovation fueled economic growth but also created systemic risk, linking credit cycles, inflation, and government debt in ways that shape our world today. This led to developments in record keeping, credit assessment

From Paper to Policy: The Age of Central Banking

As trade globalized, so did money. Governments standardized currencies, issued banknotes, and began regulating credit and interest.

By the 19th century, central banks—like the Bank of France and later the U.S. Federal Reserve (1913)—emerged to stabilize economies, issue currency, and manage crises.

Yet, the roots of their power trace directly back to banking in the Middle Ages, when trust, record-keeping, and liquidity management first became financial science.

How Historical Banking Shapes Your Finances Today

Understanding this history isn’t just trivia—it’s empowerment.

Many modern banking practices—credit scoring, interest, savings accounts, and loans—stem from ideas refined over centuries. Knowing this can help you:

-

Make smarter borrowing decisions

-

See how banks manage (and sometimes manipulate) money supply

-

Recognize how trust and regulation shape financial stability

For instance, just as medieval merchants diversified trade routes, modern investors diversify portfolios. The principles endure even as the tools evolve.

Controversial Question: Should We Return to Gold-Backed Money?

One trending debate asks: “Would a return to gold-backed money restore financial stability?”

The gold standard, once common after the Renaissance, tied currency value to physical gold. Some argue it prevents inflation; others say it limits economic flexibility.

History shows that while gold systems created stability, they also restricted growth—especially in times of crisis. The flexibility of credit and monetary policy (originating from medieval and Renaissance banking) enabled societies to rebuild after wars, pandemics, and depressions.

Takeaway: Stability requires trust, not just metal. Sound governance matters more than what backs the currency.

Downloadable Freebies

1. Timeline of Money & Banking Evolution Worksheet

Visualize the transformation of trade and finance—from bartering to digital currency.

➡️ Download the Timeline Worksheet here (insert download link on site)

2. Money Systems Through History Cheat Sheet

A one-page quick reference summarizing key milestones, from Mesopotamian temples to crypto economies.

➡️ Download the Cheat Sheet here

Internal Links

To deepen your understanding, explore related posts on TheMoneyQuestion.org:

-

The Gold Standard Debate: Should We Return To Backed Money? (Coming Soon)

- The End of Fractional Reserve Banking? Here’s What We Know

External Sources

Conclusion: The Past Is the Blueprint for the Future

The story of money and banking is the story of civilization itself. From the grain banks of Mesopotamia to the Medici in Florence, from paper notes to digital ledgers, one thing remains constant: money is a system of trust.

Understanding banking in the Middle Ages shows that our financial system—while complex—is built on simple human principles of trust, record-keeping, and mutual benefit.

Whether you’re managing a household budget or analyzing global finance, knowing where money came from helps you navigate where it’s going.

FAQs

1. What was banking in the Middle Ages like?

It revolved around merchant families, bills of exchange, and trust-based credit systems—especially in Italy and Northern Europe. It was a time of significant innovation, though practices were constrained by religious prohibitions.

2. Who were the first bankers?

This question depends on how broadly you define “banking”, as the practice evolved over thousands of years. Temples in Mesopotamia (~2000BC), The Knights Templar (12th – 13th Century), and merchants in Renaissance Italy (14th – 15th Century) are considered the world’s earliest bankers.

3. What replaced barter systems?

Commodity money—like silver, gold, and salt—eventually evolved into coins and paper money.

4. Why was usury banned in medieval Europe?

The Church viewed charging interest as immoral, though trade required credit, leading to workarounds. Bankers found ways to circumvent this ban by:

- imposing a “fine” for late repayment, with the understanding that the debtor would always pay late.

- using contracts like the bill of exchange and adjusting the exchange rate to incorporate an implicit interest payment.

5. Who invented double-entry bookkeeping?

Luca Pacioli formalized it in 1494; this system remains the foundation of modern accounting.

6. What led to the fall of the Medici Bank?

Political risk, bad loans, and mismanagement caused its collapse.

7. How did banking spread beyond Italy?

Through trade networks into France, England, and the Low Countries, setting the stage for national banks.

8. What was the first central bank?

- The world’s oldest surviving central bank, and the one widely recognized as the first, is the Sveriges Riksbank (the Swedish Riksbank). It was founded in Sweden in 1668. The Bank of England (1694) is often credited as the second central bank.

9. How did medieval banking influence today’s system?

- Medieval banking, primarily led by Italian merchant families and religious orders, provided the foundational tools and concepts that are indispensable to the modern financial system. The core contribution was the shift from a physical, coin-based economy to a credit-based, document-driven system.

10. What can modern savers learn from history?

Here are four major lessons drawn from past financial crises, economic downturns and centuries of human behaviour:

- Everyone should have a Cash Emergency Fund. Failure to have access to cash make people more vulnerable to events like The Great Depression, the 2008 financial crisis and the COVID-19 economic shock.

- Diversification across different asset classes, geographic regions and industries is a must so no single event can wipe out your entire portfolio.

- Avoid overleveraging and speculation. Be cautious with debt, especially consumer debt.

- Pay yourself first. This is the ancient discipline of thrift. Make saving automatic and non-negotiable.

Affiliate Disclosure

This post may contain affiliate links. If you purchase through these links, TheMoneyQuestion.org may earn a small commission—at no extra cost to you.

Content is for informational purposes only and not a substitute for advice from certified financial professionals.

The Tyranny of the Rate of Return

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Discover how the rate of return influences your money decisions, shapes wealth inequality, and learn strategies to break free from its hidden tyranny.

Introduction: Why “The Rate of Return” Rules Your Financial Life

When most people think about wealth, they picture hard work, budgeting, and saving. But behind the scenes, a single force quietly dictates how money grows—and who benefits most: the rate of return.

Whether it’s the interest you earn in a savings account, the growth of your retirement fund, or the yield on real estate, the rate of return acts as a financial “gravity.” It pulls wealth upward toward those who already have more, while making it harder for the average saver to catch up.

In this article, we’ll break down:

-

What the rate of return really means (and why it matters more than you think).

-

How it fuels inequality and shapes global economics.

-

Practical steps to use it for your advantage instead of being trapped by it.

By the end, you’ll understand why experts call it “the tyranny of the rate of return”—and how you can navigate it with confidence.

What Is the Rate of Return? A Simple Definition

The rate of return (ROR) is the percentage gain or loss on an investment over time.

Example:

-

You invest $1,000 in a stock.

-

A year later, it’s worth $1,100.

-

Your rate of return = (Gain ÷ Original Investment) × 100 = 10%.

ROR can apply to:

-

Savings accounts (interest earned).

-

Bonds (yield).

-

Stocks (price gains + dividends).

-

Real estate (rental income + appreciation).

It seems simple—but its long-term impact is profound.

The Power (and Tyranny) of Compounding

Albert Einstein allegedly called compound interest the “eighth wonder of the world.” But compounding works very differently depending on what rate of return you start with.

Example: Two Savers Over 30 Years

-

Saver A: Invests $10,000 with a 4% annual return → ends with about $32,000.

-

Saver B: Invests $10,000 with an 8% annual return → ends with about $100,000.

Same effort. Same time. Different access to returns. The tyranny lies in the fact that higher rates of return are easier to access if you already have wealth—through hedge funds, private equity, or real estate deals unavailable to the average worker.

The Rate of Return and Wealth Inequality

One of the most famous works on this topic is Thomas Piketty’s Capital in the Twenty-First Century. His research highlighted the formula:

r > g

-

r = the rate of return on capital.

-

g = economic growth (wages, productivity, GDP).

When the rate of return on investments consistently outpaces wage growth, wealth naturally concentrates at the top.

This is why billionaires’ fortunes grow faster than the paychecks of everyday workers. Your salary might rise 3% a year, but their portfolio grows 8–12%.

To dive deeper into inequality and money systems, see our post: Who Really Owns the Central Banks?

Trending Question: Is Chasing High Returns Always Worth It?

“Should I chase a higher rate of return?”

Many people ask whether they should pursue risky investments for higher returns. Here’s the truth:

-

Higher returns = higher risk. Crypto, meme stocks, and speculative real estate can yield double-digit returns, but they also come with the risk of major losses.

-

Moderate, steady returns build lasting wealth. A balanced portfolio of stocks, bonds, and index funds may “only” return 6–8% annually, but over decades, this creates massive compounding power.

-

Behavior matters more than the product. Avoiding panic selling, staying invested, and consistently contributing often beats the “hot tip” approach.

How Policy Shapes the Rate of Return

The rate of return is not just about personal finance—it’s shaped by larger forces:

-

Federal Reserve policies (interest rates influence bond yields and savings rates).

-

Government programs (retirement tax incentives encourage stock market participation).

-

Inflation (real return = nominal return – inflation).

For a deeper dive, read: What the Fed’s Move Means for Your Wallet.

How to Use the Rate of Return to Your Advantage

You can’t change global wealth dynamics—but you can improve your personal strategy.

1. Focus on Real Returns

If inflation is 4% and your savings account pays 2%, your real rate of return is -2%. Always consider inflation-adjusted returns.

2. Prioritize Asset Classes with Proven Returns

-

Stocks: Historically ~7–10% per year.

-

Bonds: ~3–5%.

-

Real estate: Varies, but often competitive with stocks.

3. Reduce Fees and Expenses

Even a 1% fee eats away thousands over decades. Favor low-cost index funds (like Vanguard or Fidelity).

4. Diversify

Don’t rely on one rate of return. Balance risk and stability.

5. Invest Early and Consistently

Time in the market beats timing the market.

Case Study: Two Investors and the Tyranny of Return

-

Alex: Starts investing at 25, contributes $300/month at 7% → has ~$720,000 at age 60.

-

Jordan: Starts at 35 with the same contributions and return → has ~$340,000 at age 60.

The tyranny? Same habits, different starting points. Early exposure to higher returns matters.

Authoritative References

-

U.S. Securities and Exchange Commission (SEC): Compound Interest

-

National Bureau of Economic Research: Capital and Wealth Inequality

FAQs: The Rate of Return Explained

1. What is a good rate of return on investments?

Historically, 7–10% annually in stocks is considered strong.

2. How does inflation affect the rate of return?

It reduces your real return. If inflation = 5% and your return = 6%, your real return = 1%.

3. Why do the wealthy get higher rates of return?

They access private investments, have tax advantages, and can take more risks.

4. What is the average rate of return on a 401(k)?

Commonly cited averages fall in the range of 5% to 8% annually, assuming a balanced or moderate-risk portfolio (mix of stocks and bonds). Investopedia

5. Is the rate of return guaranteed?

No—returns vary based on risk, market, and time horizon.

6. Should I invest in bonds if they have a lower rate of return?

Yes, for stability. Bonds balance out volatile assets.

7. How can I improve my rate of return safely?

Focus on low-cost index funds, diversify, and start early.

8. What is the difference between nominal and real rate of return?

Nominal = raw return. Real = adjusted for inflation.

9. Does compounding make a big difference?

Yes, small differences in return lead to massive wealth gaps over decades.

10. Can I retire with a 4% rate of return?

Yes, but it requires larger savings contributions compared to someone earning 8%.

Conclusion: Don’t Be Ruled by the Tyranny of the Rate of Return

The rate of return shapes not just your personal wealth but the broader global economy. While you can’t control market dynamics or systemic inequality, you can control how you respond:

-

Start early.

-

Stay consistent.

-

Focus on real, inflation-adjusted returns.

-

Cut costs and fees.

By understanding and working with the forces of compounding, you’ll put yourself in the best position to thrive—even in a system where the rate of return seems stacked against you.

Affiliate Disclosure

Some links in this article may be affiliate links. If you click and make a purchase, TheMoneyQuestion.org may earn a commission at no additional cost to you. This content is for informational purposes only and is not a substitute for professional financial advice from a licensed advisor.

Banking Regulations Explained: How New Policies Affect Your Money

{kind=link}

AFFILIATE DISCLOSURE:

This article contains affiliate links. We may receive a commission for purchases made through these links, at no extra cost to you. We only recommend products and services we believe will genuinely help you achieve your financial goals.

Learn how 2024 banking regulations—from overdraft fees to open banking—affect your money and what you can do to adapt.

Introduction

Banking regulations are crucial in maintaining financial stability, ensuring consumer protection and promoting fair practices in the financial sector. However, frequent policy changes can leave consumers confused about how these rules impact their money.

This comprehensive guide will explain the latest banking regulations and their implications for your finances Here is a clearer version of the text:

“and offer practical insights to help you adapt to these changes.”

Why Banking Regulations Matter

Banking regulations are laws and guidelines government agencies impose to oversee financial institutions. These rules aim to:

- Protect consumers from unfair practices.

- Ensure financial stability by preventing bank failures.

- Promote transparency in banking operations.

- Combat fraud and money laundering.

Key regulatory bodies include:

- Federal Reserve (Fed) – Oversees monetary policy and bank stability.

- Federal Deposit Insurance Corporation (FDIC) – insures deposits and supervises banks.

- Consumer Financial Protection Bureau (CFPB) – Protects consumers from predatory financial practices.

- Office of the Comptroller of the Currency (OCC) – Regulates national banks.

Recent Changes in Banking Regulations

- Stricter Capital Requirements (Basel III Endgame)

The Basel III reforms, implemented globally, require banks to hold more capital to absorb losses during economic downturns. The U.S. Federal Reserve’s “Basel III Endgame” proposal further tightens these rules for large banks.

How It Affects You: